, Shuiting Wu 2,*

, Shuiting Wu 2,*

1 School of Economics, Guangxi University, 530004 Nanning, Guangxi, China

2 School of International Economics and Political Science, Guangxi University of Finance and Economics, 530003 Nanning, Guangxi, China

Abstract

In the context of the Chinese government’s emphasis on party leadership of state-owned enterprises (SOEs), we examine the effect of party organization governance on internal control quality by employing a difference-in-differences model. We find that party organization governance significantly improves SOEs’ internal control quality. Reducing corporate violations, inhibiting earnings manipulation, and curbing on-the-job consumption are the main channels through which party organization governance enhances internal control quality. The positive effect is more pronounced for firms with lower executive shareholding and lower analyst attention. We revisit the role of party organization governance in emerging markets from the perspective of internal control quality.

Keywords

- party organization governance

- state-owned enterprises

- internal control quality

- difference-in-differences model

According to the Chinese National Bureau of Statistics (https://data.stats.gov.cn/easyquery.htm?cn=C01) and the Ministry of Finance (https://www.gov.cn/xinwen/2023-01/30/content_5739270.htm), the gross domestic product of State-owned enterprises (SOEs) accounted for 68.1% of the gross national product in 2023, indicating that SOEs play an important role in the Chinese economy. A sound internal control system is crucial for ensuring the steady development of SOEs. Since 2012, the Chinese government has endeavored to strengthen the internal control systems of SOEs to prevent business risks. After years of construction and development, the internal control system of SOEs has laid a solid micro-foundation for the steady operation of the national economy (Han et al., 2022). However, internal control practices in SOEs still reveal numerous weaknesses, as shown by negative audit opinions on internal control reports published every year, thereby increasing SOEs’ development risks. As a result, the government has continued to introduce a series of policies to improve internal control and strengthen the risk resilience of SOEs. With the introduction of these policies and the publication of related cases, numerous scholars have grown increasingly interested in the factors affecting the effectiveness of internal control.

Prior literature mainly focuses on the impact of qualified foreign institutional investors (Li et al., 2021), social trust (Liu et al., 2022), institutional environment (Chen et al., 2022), executive pay gap (Han et al., 2022) and Chief Executive Officer (CEO) background (Ge and Xiong, 2023) on internal control quality. These findings indicate that corporate governance is closely related to internal control quality. However, existing studies have largely overlooked the role of the communist party organization—an important feature of Chinese SOEs’ governance structure—on internal control quality (Shen et al., 2021; Liu et al., 2022). Especially in China, where capital markets remain underdeveloped, party organization governance may greatly affect the quality of internal control. Only a few scholars have directly studied the impact of party organization governance on internal control quality. For example, Yan et al. (2024b) argue that embedding party members within management significantly improves internal control quality. Unfortunately, their study does not reveal the impact of the Chinese government’s new initiative to establish the legal governance status of party organizations on internal control quality, nor does it clarify the channels through which party organization governance affects internal control quality.

Within the unique Chinese economic system, the communist party organization’s participation in SOE corporate governance is highly prevalent. The Chinese government has continued to improve the scope and means of party organization participation in SOEs’ corporate governance. In particular, the Chinese government issued the Regulations on the Work of the Party Group of the Communist Party of China (for Trial Implementation) for central SOEs in 2015, and the Notice on the Issuance of the Key Tasks for Implementing the Spirit of the National Conference on Party Building Work of State-owned Enterprises promulgated for all SOEs in 2016, which stipulated that major decisions, major personnel appointments and dismissals, major project arrangements, and the use of large funds (“Three Major and One Large” matters) must be pre-discussed by the communist party organizations before the directors and executives make decisions (Lin and Milhaupt, 2021). That is the communist party organization’s “pre-discussion” decision-making mechanism (CPOPD decision-making mechanism), which forms a new party organization governance model by incorporating party leadership into the governance structure of SOEs.

Thus, we consider the policies enacted in 2015 and 2016 as exogenous shocks. Using a sample of A-share listed firms in Shanghai and Shenzhen from 2012–2022, we employ a difference-in-differences (DID) approach to investigate the effect of party organization governance formed by the CPOPD decision-making mechanism on internal control quality. Based on the specific scope and operational path of the CPOPD decision-making mechanism, we reveal the underlying mechanisms through which party organization governance affects internal control quality. Moreover, considering that the governance role of the Communist Party organization may be affected by corporate internal and external governance structures, we combine internal and external governance perspectives to further examine the heterogeneous effects of party organization governance on the internal control quality of firms with different executive shareholdings and analyst attention. Our study expands the relevant literature on party organization governance and internal control quality, providing a theoretical foundation for future research.

We focus on internal control quality in Chinese firms for the following reasons. First, China is the world’s largest developing country (Shang et al., 2023), plays an influential role in the global economy and is one of the most important investment destinations (Chen et al., 2022; Lin et al., 2022). It is critical for investors worldwide to understand internal control quality and the factors that influence it in Chinese listed firms. Second, the Chinese government has emphasized construction of internal control systems in firms after the outbreak of a series of accounting scandals (Li et al., 2019; Han et al., 2022). Moreover, a series of regulations was proposed to establish and improve the internal control system. As an essential part of emerging markets, China has a weak market base like other emerging economies. It is instructive to study the Chinese government’s policy on constructing internal control systems as a reference for listed firms in other emerging economies. Third, there is a unique corporate governance system in China, which differs from the modern Western corporate governance model (Bi, 2021; Xie et al., 2022). Especially in the context of the Chinese government’s emphasis on party leadership in SOEs, the government has enacted a series of policies to optimize the Communist Party organizations’ involvement in SOE corporate governance, providing an ideal natural experiment to study the impact of China’s unique corporate governance model on internal control quality.

The main contributions of our study are as follows. First, we add to the corporate governance literature by studying party organization governance formed by the CPOPD decision-making mechanism, which formally establishes the legitimate governance status of party organization, on internal control quality. To our knowledge, only three papers discuss this policy. Lin and Milhaupt (2021) discuss the circumstances surrounding resistance to implementing the CPOPD decision-making mechanism. Xie et al. (2022) find that the politicization of corporate governance positively impacts SOEs’ stock prices and market values. Wang et al. (2025) examine the impact of political control on internal governance in SOEs. Since the outbreak of the Enron and WorldCom scandals, governments have emphasized the importance of internal control systems. In China, the government has considered it an important development goal to improve the internal control system and enhance the risk resistance of SOEs (Han et al., 2022). Therefore, SOE internal control quality deserves more attention than stock prices and market values. Accordingly, we investigate the effect of party organization governance formed by the CPOPD decision-making mechanism on internal control quality, filling a gap in the existing literature. Our findings provide both Chinese experience and a policy-making reference for the innovation of corporate governance models in developing countries (regions).

Second, we comprehensively analyze the mechanism through which party organization governance affects internal control quality from institutional theory and agency theory, broadening theoretical perspectives on internal control quality. Previous literature primarily examines the mechanisms of agency costs in corporate governance structures affecting internal control quality based on agency theory. In contrast to existing literature, we illuminate the compulsory and regulatory characteristics of party organization governance formed by the CPOPD decision-making mechanism from the perspective of institutional theory. Furthermore, integrating agency theory, we demonstrate that the pre-discussion of major matters by party organizations can improve internal control quality by reducing corporate violations, inhibiting earnings manipulation, and curbing on-the-job consumption. research expands and deepens understanding of the underlying mechanisms through which party organization governance affects internal control quality from institutional theory and agency theory, providing theoretical support for future research.

Third, the role of party organization governance varies according to different internal and external governance levels. We explore the heterogeneous effects of party organization governance on internal control quality in firms with different executive shareholdings and firms with different analyst attention. Our findings confirm the effectiveness of party organization governance in firms with weak internal and external governance in terms of improving internal control quality, providing valuable insights for optimizing party organization governance under different internal and external governance environments.

The remainder of this paper is organized as follows. Section 2 reviews relevant literature and develops our hypotheses. Section 3 describes the empirical methods. Section 4 reports empirical results and robustness tests. Section 5 examines the mechanisms. Section 6 provides a heterogeneity analysis. Section 7 concludes.

In many countries, especially developing countries, governments play a vital role in corporate decision-making (Boubakri et al., 2012). Within China’s unique economic system, the government often intervenes in firms’ operational decisions by strengthening the involvement of Communist Party organizations in corporate governance. There are two strands of literature closely related to our research.

One stream of literature explores the effect of party organization governance. Extensive research demonstrates that party organizations’ participation in corporate governance contributes to improving investment efficiency (Li et al., 2020), curbing executive corruption (Yuan et al., 2023), and weakening managerial power (Wang et al., 2023), thereby significantly promoting corporate performance (Xie et al., 2022) and enhancing corporate innovation (Lin et al., 2023). Few studies examine the impact of party organization embedded on internal control quality. For instance, Yan et al. (2024b) adopt the proportion of party members on the board of directors, senior executives, and supervisory board to measure party organization governance, finding that party organization governance promotes internal control quality.

Another stream of literature examines the determinants and economic effects of internal control quality. Many scholars point out that executive compensation (Balsam et al., 2014; Han et al., 2022), executive characteristics (Lin et al., 2014; Shen et al., 2021), executive backgrounds (Ge and Xiong, 2023), board structure (Chen et al., 2017; Hu et al., 2017), shareholding structure (Li et al., 2021), social trust (Liu et al., 2022), and institutional environments (Chen et al., 2022) are important factors affecting internal control quality. Other scholars investigate the impact of internal control on the credit spread on publicly traded debt (Dhaliwal et al., 2011), changes in suppliers’ or customers’ relationship-specific investments (Lai, 2019), corporate research and development (R&D) investment (Li et al., 2019), and corporate environmental, social, and governance (ESG) information disclosure (Yan et al., 2024a).

Existing literature has conducted extensive research on the impact of party organization governance and on the determinants and economic consequences of internal control quality. However, there is little literature that directly examines the relationship between party organization governance and internal control. Yan et al. (2024b) examine the impact of party organization embedded on internal control, but their focus is neither on party organization governance formed by the CPOPD decision-making mechanism nor on revealing the underlying mechanisms through which party organization governance affects internal control quality. We first consider the CPOPD decision-making mechanism as an exogenous shock and examine the impact of party organization governance on internal control quality, thereby improving and expanding the relevant literature. Second, we combine institutional theory and agency theory to reveal the underlying mechanisms through which party organization governance affects internal control quality, thereby providing a theoretical foundation for future research. Third, we further explore the heterogeneous role of party organization governance at different levels of internal and external governance, providing empirical references for improving party organization governance.

The main theoretical support for party organization governance effects comes from institutional theory and agency theory. Institutional theory focuses on the interaction between institutions and organizations and emphasizes the constraining and regulating roles of formal institutions on firm behavior (Zhou et al., 2017). The CPOPD decision-making mechanism, as a formal institutional arrangement for the party organization’s participation in the corporate governance of SOEs, empowers party organizations to participate in major decisions and emphasizes the legitimate status of the party organization as an internal supervisor. Party organization governance formed by the CPOPD decision-making mechanism is conducive to improving major decision-making procedures, strengthening the internal supervision mechanism, and thereby improving the internal control quality of SOEs. Agency theory indicates that the separation of ownership and management leads to serious agency problems (Jensen and Meckling, 1976), which affect firms’ internal control. For example, Zhang et al. (2020) and Han et al. (2022) indicate that SOEs with dual principal-agent problems may have internal control deficiencies. Accordingly, the CPOPD decision-making mechanism establishes the legal status of party organizations as internal governance subjects, providing a normative foundation for their participation in SOE governance. As an important supplement to traditional governance forces, party organizations can effectively mitigate agency conflicts in SOEs by participating in the decision-making process for “Three Major and One Large” matters, thereby enhancing internal control quality.

More specifically, party organization governance formed by the CPOPD decision-making mechanism can improve internal control quality in three aspects. First, the CPOPD decision-making mechanism clearly stipulates that major matters must be discussed in advance by party organizations before being decided by management. Party organizations evaluate compliance risks and potential consequences during the discussion, thereby reducing corporate violations at the source and improving the quality of internal control. For instance, in 2017, the Jinan Culture and Tourism Development Group in Shandong Province suffered from excessive venture capital and severe loss of state-owned assets due to non-standard deliberation system and procedures of the party organization. After 2023, the group strictly implemented the CPOPD decision-making mechanism, effectively reduced illegal decision-making, and significantly increased corporate profits. Second, party organizations can gain greater access to internal business information through direct participation in major business decisions, significantly reducing information asymmetry between supervisors and operators. Therefore, party organization governance can curb earnings manipulation of executives who take advantage of inside information for personal interests, subsequently strengthening internal control quality. Third, the participation of the party organization in the decision-making of the “Three Major and One Large” matters can not only reduce management’s discretionary power over the firm’s resources but also strengthen the supervision of executives’ behavior, effectively curbing on-the-job consumption of management (Guo et al., 2019). Xie et al. (2022) believe that political governance formed by integrating party leadership into the corporate governance structure may significantly curb executive corruption.

Based on the above analysis, the CPOPD decision-making mechanism legitimizes the embedding of party organizations and establishes formalized decision-making procedures through explicit institutional arrangements, providing an institutional foundation for party organization governance. As internal supervisors, party organizations can effectively reduce corporate violations, inhibit earnings manipulation, and curb on-the-job consumption through pre-discussion of major matters, thereby improving internal control quality. Therefore, we propose the following hypothesis:

H1. Party organization governance can improve internal control quality.

Incentive compatibility refers to aligning the interests of executives with those of the firm, enabling executives to work hard for their own benefit while maximizing the interests of the firm. Executive equity incentives can bind executive interests to firm value. Internal control quality is closely related to firm value (Beneish et al., 2008). Kim et al. (2011) identify that internal control deficiencies lead to higher capital costs and more negative credit ratings, thereby decreasing firm value. Since internal control deficiencies negatively impact executive wealth, executives have a stronger motivation to improve internal control in firms with more executive shareholding. In particular, executives may work harder to increase their wealth by increasing firm value. Moreover, executives may reduce violations, earnings manipulation, and corrupt behavior to avoid stock price declines triggered by the disclosure of internal control deficiencies. However, executives cannot derive excess returns from favorable firm performance without adequate equity incentives. As a result, executives may construct poor internal control and attempt to extract firm value for personal gain. According to the above analysis, we expect party organization governance formed by the CPOPD decision-making mechanism to play a limited role in firms with more executive shareholding. However, party organization governance in firms with lower executive shareholding tends to be more strongly associated with greater internal control quality. This argument leads to the following hypothesis:

H2. Compared with firms with more executive shareholding, the positive effect of party organization governance on internal control quality is more significant in firms with lower executive shareholding.

Corporate governance theory emphasizes that the improvement of corporate governance efficiency depends on the collaborative effect of internal and external governance mechanisms. Analysts, an important external supervisory force, play an external governance role by directly monitoring or attracting investors to scrutinize the behavior of corporate managers (Xie et al., 2024). On the one hand, analysts directly supervise executives by collecting private information, screening executives and the governance system of the companies they cover, and rating corporate governance (Lehmann, 2019). In this situation, executives realize that any violations may be disclosed by analysts, prompting them to proactively reduce violations and construct sound internal control to achieve a higher corporate governance rating (Huang et al., 2020). On the other hand, analysts transmit abundant corporate information to external stakeholders through ratings and reports, which can not only strengthen the supervision and restraint by external investors over executives, but also mitigate information asymmetry, thus reducing the risk of executives taking advantage of their informational advantage to engage in earnings manipulation and on-the-job consumption (Liu et al., 2021; Xie et al., 2024). In contrast, outside investors can rarely acquire critical internal information from professional analyst reports in firms with lower analyst attention. Low information transparency makes it difficult for outside shareholders to monitor and discipline executive behavior effectively. In this case, executives are inclined to build weak internal control systems to gain more private benefits. Consequently, we argue that party organization governance formed by the CPOPD decision-making mechanism may play a more significant role in improving internal control quality for firms with lower analyst attention than those with more analyst attention, as it can compensate for the shortcomings of the external market governance mechanism. This gives rise to the following research hypothesis:

H3. Compared with firms with more analyst attention, the positive effect of party organization governance on internal control quality is more significant in firms with lower analyst attention.

We adopt a firm-level sample from Chinese A-share listed firms in Shanghai and Shenzhen from 2012 to 2022. According to the regulations of the Chinese Ministry of Finance, all main board-listed companies were required to construct an internal control system starting in 2012. Thus, we select 2012 as the starting point to increase the reliability of our findings. We use the following criteria for sample selection. First, we eliminate financial firms as defined in the China Securities Regulatory Commission’s 2012 classification, insolvent firms, and special treatment (ST) and *ST firms. Second, to enhance the accuracy of the empirical study, we supplement the data on firms missing ownership-type information by searching annual reports. Third, we exclude firms listed after 2012. Fourth, we remove samples with missing values for the dependent, independent, and control variables. The final sample contains 2113 firms with 20,564 firm-year observations. We obtain internal control index score from the DIB Internal Control and Risk Management Database, which is widely used and cited by Chinese scholars, firms, and media. The data on the implementation of the CPOPD decision-making mechanism in SOEs is derived from the company’s charter. In addition, the relevant financial data is obtained from the China Stock Market and Accounting Research (CSMAR) database and listed firms’ annual reports.

Internal control quality (IC). Internal control is an institutional arrangement that enables firms to comply with relevant laws and regulations, ensures reliable financial reporting, and ultimately achieves operational objectives. The DIB internal control index is constructed based on the implementation effectiveness of corporate development strategy, operational returns, the integrity of financial information disclosure, legal compliance, and asset security, and serves as an important indicator of the quality of internal control in Chinese listed companies (Liu et al., 2022). Following Li et al. (2021) and Shen et al. (2021), we employ the DIB internal control score to measure internal control quality. The original value of the DIB internal control score ranges from 0 to 1000. To alleviate concerns about the relatively dispersed distribution of the index, we adopt the same normalization method as Shen et al. (2021) and divide the DIB internal control score by 1000 to create a proxy variable for corporate internal control quality.

The independent variable is party organization governance (Party). Following Xie et al. (2022) and Wang et al. (2025), we define party organization governance (Party) as a dummy variable indicating whether firms amended their articles of association to implement the CPOPD decision-making mechanism in year t. For firms that amended their articles of association to implement the CPOPD decision-making mechanism in year t, Party is equal to one in that year and subsequent years, and zero otherwise.

The guiding opinions issued by the Chinese government require SOEs to incorporate the CPOPD decision-making mechanism into the articles of association to expressly grant the party’s leadership and party organizations formal legal status within the firm. To implement the CPOPD decision-making mechanism, a model template for amending corporate articles of association amendments was publicly circulated (Lin and Milhaupt, 2021). We obtain data for the independent variable from the articles of association announced on the Juchao website (http://www.cninfo.com.cn/new/index), a listed firm information disclosure website designated by the China Securities Regulatory Commission that contains official announcements from all Chinese listed firms (Xie et al., 2022). A firm’s articles of association are its foundational legal documents, specifying its name, domicile, scope of business, business management system, and other important matters, along with the basic organizational rules and procedures. We manually query the announcements of listed firms regarding amendments to articles of association from 2015 to 2022 to identify whether the firm amended its articles of association to implement the CPOPD decision-making mechanism and the year in which the amendment first occurred. Notably, once firms initially amended their articles of association to implement the CPOPD decision-making mechanism in a given year, they continued its implementation in subsequent periods.

According to Shen et al. (2021), we control for a series of variables that affect corporate internal control quality, including firm size (Size), profitability (ROA), monetary funds (Cash), financial leverage (Leverage), the operating income growth rate (Growth), the total number of board members (Bsize), the ratio of independent directors (Indb), the ratio of shares held by the largest shareholder (Largest), whether the general manager and chairman is the same person (Dual), the number of board meetings (Meeting), and whether the firm is audited by one of the Big Four accounting organizations (Big4).

All non-binary variables are winsorized at the 1st and 99th percentiles to minimize the effect of outliers. Table 1 lists the symbols and specific definitions of the main variables in this paper.

| Symbols | Definitions |

| IC | The DIB internal control score divided by 1000. |

| Party | A dummy variable indicating whether firms amended their articles of association to implement the CPOPD decision-making mechanism in year t. For firms that amended their articles of association to implement the CPOPD decision-making mechanism in year t, Party is equal to one in that year and subsequent years, and zero otherwise. |

| Size | The natural logarithm of total book-value assets. |

| ROA | Return on total assets. |

| Cash | The natural logarithm of monetary funds. |

| Leverage | Total debt divided by total assets. |

| Growth | The operating income growth rate. |

| Bsize | The natural logarithm of the total number of board members. |

| Indb | The number of independent directors divided by the total number of board members. |

| Largest | The number of the largest shareholder’s shares divided by the total share capital. |

| Dual | General manager and chairman of the same person is one, otherwise it is zero. |

| Meeting | The natural logarithm of the number of board meetings. |

| Big4 | A dummy variable equal to one if the external auditor is a Big4 accounting firm, and zero otherwise. |

Notes: The table lists the symbols and specific definitions of the main variables in this paper. CPOPD, communist party organization’s “pre-discussion”.

Table 2 shows descriptive statistics of internal control quality and other variables used in our primary analyses for the treatment group and control group, respectively. The average internal control quality (IC) in the treatment and control groups is 0.6415 and 0.6258, with a minimum of 0 and a maximum of 0.8332. This suggests the presence of a considerable gap in the internal control quality of Chinese listed firms.

| Variables | N | Mean | STD | Min | Median | Max | |

| Panel A: Treatment group | |||||||

| IC | 8970 | 0.6415 | 0.1366 | 0.0000 | 0.6668 | 0.8332 | |

| Size | 8970 | 23.0101 | 1.3962 | 19.9225 | 22.8906 | 26.5158 | |

| ROA | 8970 | 0.0280 | 0.0509 | –0.2574 | 0.0267 | 0.1885 | |

| Cash | 8970 | 20.9605 | 1.4597 | 17.2222 | 20.8766 | 24.6066 | |

| Leverage | 8970 | 0.5090 | 0.1986 | 0.0590 | 0.5179 | 0.9073 | |

| Growth | 8970 | 0.1159 | 0.3754 | –0.5912 | 0.0672 | 2.6123 | |

| Bsize | 8970 | 2.2837 | 0.2359 | 1.6094 | 2.1972 | 2.8332 | |

| Indb | 8970 | 0.3741 | 0.0565 | 0.3333 | 0.3636 | 0.5714 | |

| Largest | 8970 | 0.3894 | 0.1472 | 0.0832 | 0.3783 | 0.7380 | |

| Dual | 8970 | 0.0963 | 0.2950 | 0.0000 | 0.0000 | 1.0000 | |

| Meeting | 8970 | 2.2178 | 0.3800 | 1.3863 | 2.1972 | 3.1781 | |

| Big4 | 8970 | 0.1000 | 0.3000 | 0.0000 | 0.0000 | 1.0000 | |

| Panel B: Control group | |||||||

| IC | 11,594 | 0.6258 | 0.1424 | 0.0000 | 0.6575 | 0.8332 | |

| Size | 11,594 | 22.1919 | 1.1859 | 19.9225 | 22.0808 | 26.5158 | |

| ROA | 11,594 | 0.0313 | 0.0688 | –0.2574 | 0.0336 | 0.1885 | |

| Cash | 11,594 | 20.2133 | 1.3115 | 17.2222 | 20.1435 | 24.6066 | |

| Leverage | 11,594 | 0.4078 | 0.1993 | 0.0590 | 0.4001 | 0.9073 | |

| Growth | 11,594 | 0.1638 | 0.4351 | –0.5912 | 0.0942 | 2.6123 | |

| Bsize | 11,594 | 2.1796 | 0.2341 | 1.6094 | 2.1972 | 2.8332 | |

| Indb | 11,594 | 0.3770 | 0.0528 | 0.3333 | 0.3636 | 0.5714 | |

| Largest | 11,594 | 0.2989 | 0.1390 | 0.0832 | 0.2778 | 0.7380 | |

| Dual | 11,594 | 0.3210 | 0.4669 | 0.0000 | 0.0000 | 1.0000 | |

| Meeting | 11,594 | 2.2202 | 0.3846 | 1.3863 | 2.1972 | 3.1781 | |

| Big4 | 11,594 | 0.0461 | 0.2096 | 0.0000 | 0.0000 | 1.0000 | |

Notes: The table shows the results of descriptive statistics for the main variables. STD, standard deviation.

Following Hu et al. (2023), we construct the following empirical model to investigate the effect of party organization governance formed by the CPOPD decision-making mechanism on internal control quality using a difference-in-differences approach.

where, the subscripts i and t denotes the firm and year, respectively.

ICit represents internal control quality. Partyit denotes party

organization governance. Controlsit denote a series of control variables,

Table 3 presents the estimates of internal control quality. Column (1) contains only Party, firm- and year-fixed effects. In column (2), all control variables are added to the specifications in column (1). The estimated coefficients of Party in columns (1) and (2) are all significantly positive at the 1% level, suggesting that our estimates are robust. The estimated coefficient of Party in column (2) is 0.0141, indicating that party organization governance formed by the CPOPD decision-making mechanism induces a 0.0141 increase in the IC coefficient, implying that party organization governance corresponds to a 14.10 increase in the corporate internal control index score, representing a substantial improvement in internal control quality (Hypothesis 1 (H1) is supported). To measure the economic significance of this result, we compare the estimated coefficient to the standard deviation of the corporate internal control quality. The standard deviation for the IC is 0.1366 in the treatment group, as shown in Panel A of Table 2, suggesting that party organization governance explains about 10.32% (0.0141/0.1366) of the variation in internal control quality. These findings indicate that party organization governance can reduce corporate violations, inhibit earnings manipulation, and curb executive on-the-job consumption, thereby improving the internal control quality in SOEs.

| (1) | (2) | |

| IC | IC | |

| Party | 0.0280*** | 0.0141*** |

| (0.0041) | (0.0037) | |

| Size | 0.0105** | |

| (0.0042) | ||

| ROA | 0.6324*** | |

| (0.0315) | ||

| Cash | 0.0072*** | |

| (0.0024) | ||

| Leverage | –0.0259* | |

| (0.0152) | ||

| Growth | 0.0220*** | |

| (0.0027) | ||

| Bsize | –0.0182*** | |

| (0.0060) | ||

| Indb | –0.0075 | |

| (0.0305) | ||

| Largest | 0.0589*** | |

| (0.0190) | ||

| Dual | 0.0062* | |

| (0.0034) | ||

| Meeting | –0.0056* | |

| (0.0032) | ||

| Big4 | 0.0023 | |

| (0.0094) | ||

| Firm FE | Yes | Yes |

| Year FE | Yes | Yes |

| Constant | 0.6779*** | 0.3177*** |

| (0.0026) | (0.0720) | |

| N | 20,564 | 20,564 |

| Adj. R2 | 0.0320 | 0.1360 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively. FE, Fixed Effects.

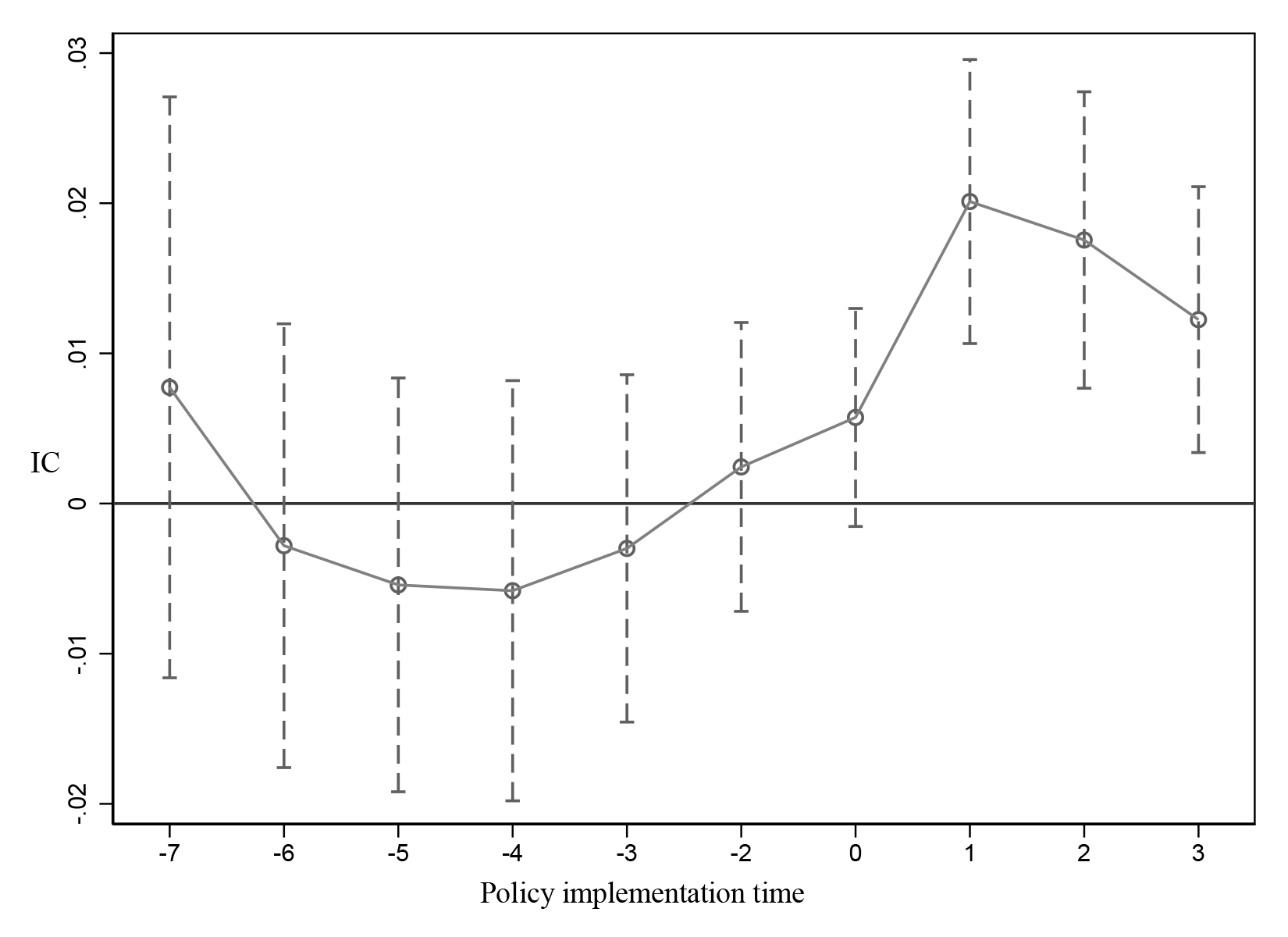

To analyze the premise of parallel trends between treatment and control groups and to assess the dynamic effects of party organization governance formed by the CPOPD decision-making mechanism on internal control quality, we follow Beck et al. (2010) and construct the following model:

In model (2),

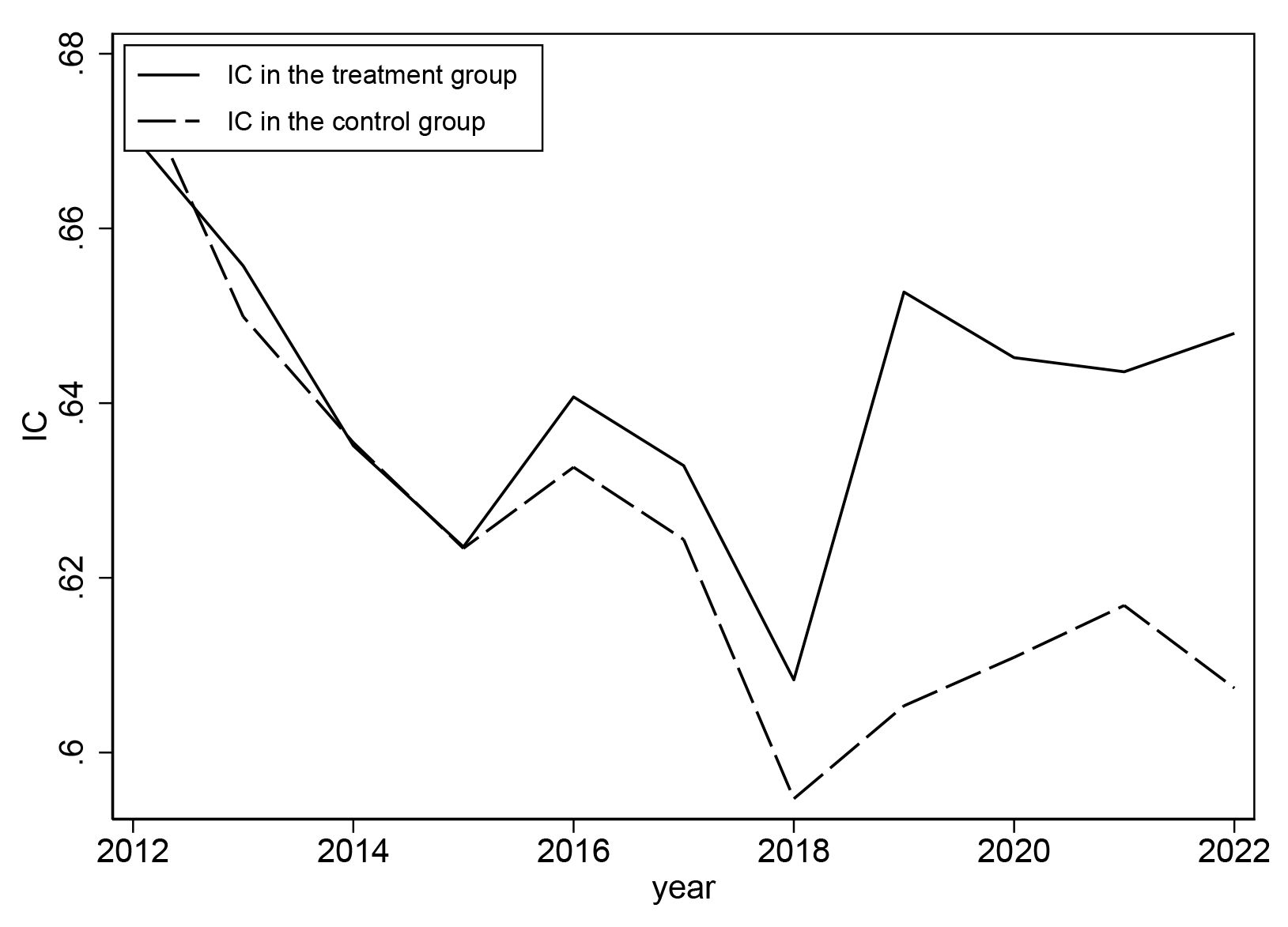

Fig. 1 shows model (2) estimation results with 95% confidence intervals. According to Fig. 1, the coefficients of Party are insignificantly different from zero for all years before the CPOPD decision-making mechanism implementation, indicating that internal control quality was not significantly different between the treatment group and control group. In other words, we cannot reject the assumption of parallel trends beforehand. In addition, we plot the DIB internal control score divided by 1000 for the treatment and control groups to visualize changes in internal control quality in the treatment and control groups before and after the policy shock in Appendix Fig. 3. The insignificant differences between the treatment and control groups before implementing the CPOPD decision-making mechanism confirm the visual inspection of the parallel trend. Since the Chinese government issued the policy document on the CPOPD decision-making mechanism in 2015, there has emerged a difference in internal control quality between the treatment group and the control group. With the increase in the number of firms implementing the CPOPD decision-making mechanism, the difference has grown increasingly significant.

Fig. 1.

Fig. 1.

Parallel trends and dynamic effects.

Moreover, the regression coefficients of Party are significantly positive and decline steadily in the first year and the following years after implementing the CPOPD decision-making mechanism, indicating that party organization governance formed by the CPOPD decision-making mechanism significantly improves the quality of internal control, and the improvement effect decreases gradually. Hypothesis 1 (H1) is confirmed. Notably, the estimated coefficients are insignificant at the year of implementation of the CPOPD decision-making mechanism because there is a lag between the government’s promulgation of policy and the firms’ actual implementation.

We perform two-stage least squares estimations with an instrumental variable to address endogeneity. Following Zhang et al.’s (2023) approach to constructing the instrumental variable, we use the proportion of firms implementing the CPOPD decision-making mechanism relative to the total firms in the same industry in the same year (Partyp). The higher the implementation rate within the industry, the greater the pressure on a firm to implement. However, the implementation ratio within the industry has no direct impact on internal control quality within a firm. Table 4 reports the estimated results. The first-stage regression result in column (1) shows that the instrumental variable Partyp is significantly positively correlated with party organization governance, suggesting that the instrumental variable has strong explanatory power for the independent variable. The result of the second stage in column (2) reveals that the independent variable is statistically significantly positive. Furthermore, the CD F-statistics used to test weak instrumental variables are significantly higher than the conventional critical value of 10. As shown in Table 4, party organization governance still significantly improves internal control quality even after employing instrumental variables to mitigate endogeneity.

| (1) | (2) | |

| Party | IC | |

| Partyp | 3.1792*** | |

| (0.1800) | ||

| Party | 0.0305*** | |

| (0.0110) | ||

| Size | –0.0746* | 0.0132*** |

| (0.0403) | (0.0015) | |

| ROA | –0.4144 | 0.7297*** |

| (0.4093) | (0.0165) | |

| Cash | 0.2458*** | 0.0083*** |

| (0.0344) | (0.0013) | |

| Leverage | 1.0912*** | –0.0416*** |

| (0.1471) | (0.0057) | |

| Growth | –0.1596** | 0.0182*** |

| (0.0644) | (0.0022) | |

| Bsize | 1.1259*** | –0.0284*** |

| (0.0991) | (0.0040) | |

| Indb | 4.4315*** | 0.0063 |

| (0.1730) | (0.0082) | |

| Largest | –1.2580*** | 0.0091*** |

| (0.0675) | (0.0025) | |

| Dual | –0.1556** | –0.0103*** |

| (0.0632) | (0.0024) | |

| Meeting | –0.2749*** | 0.0110*** |

| (0.0887) | (0.0037) | |

| Big4 | –0.0746* | 0.0132*** |

| (0.0403) | (0.0015) | |

| Firm FE | Yes | Yes |

| Year FE | Yes | Yes |

| CD F statistic | 1259.087 | |

| Constant | –9.0156*** | 0.2876*** |

| (0.5032) | (0.0214) | |

| N | 12,859 | 20,564 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively.

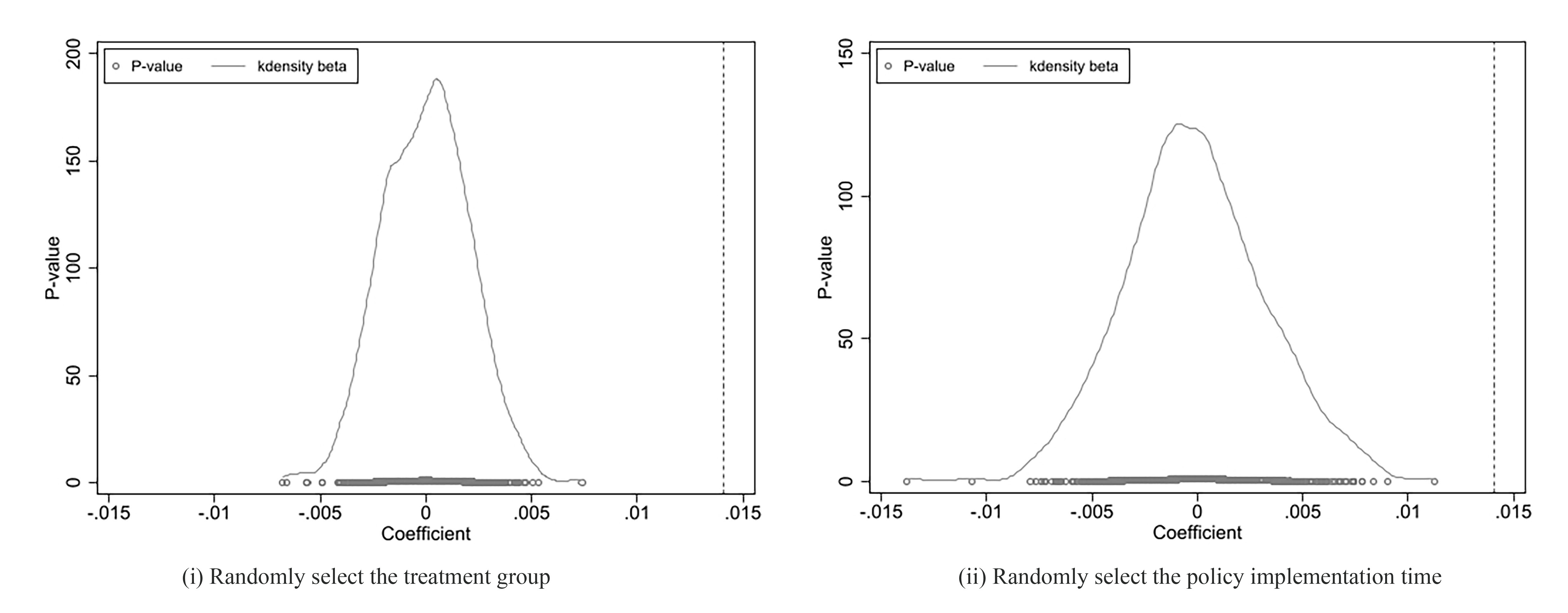

We employ placebo tests to ensure that the improvement effect of party organization governance on internal control quality is not driven by random chance. First, we randomly select a treatment group that implemented the CPOPD decision-making mechanism from the total sample to construct pseudo-treatment samples and randomly select the policy implementation time to construct false policy implementation variables following Chen and Xie (2022). Next, we repeat the above process 500 times and plot the estimated coefficients for the 500 placebo tests, the corresponding p-values, and the estimated coefficients obtained from the baseline regression (column (2) of Table 3) in (i) and (ii) of Fig. 2. According to Fig. 2, the estimated coefficients of the placebo test are mainly concentrated around zero and distinct from those of the benchmark regression, thereby ruling out the possibility that random factors drive the findings.

Fig. 2.

Fig. 2.

The results of the placebo tests based on random selection of the treatment group and the policy implementation time. (i) Placebo test with random selection of the treatment group. (ii) Placebo test with random selection of the policy implementation time.

The sample period in our study overlaps with major policy reforms, which may interfere with the estimation results. Therefore, we conduct a detailed review of other relevant policies that may affect internal control quality during the sample period and identify the following three initiatives which could bias the results. Specifically, the Chinese government implemented the anti-corruption campaign in 2013; prohibited government officials from serving as independent directors in 2014 (with the policy formally issued in October 2013 and effective from 2014); and initiated the classified promotion of mixed-ownership reform of SOEs in 2015. These policies may affect internal control quality of SOEs. Therefore, we construct these policies implementation variables SOE13, SOE14, and SOE15 in the same manner as the independent variable and add them to model (1) for estimation. The results in Table 5 show that, after controlling relevant policies, party organization governance still significantly improves the internal control quality of SOEs.

| (1) | (2) | (3) | |

| IC | IC | IC | |

| Party | 0.0128*** | 0.0138*** | 0.0120*** |

| (0.0037) | (0.0039) | (0.0041) | |

| SOE13 | 0.0072 | ||

| (0.0051) | |||

| SOE14 | 0.0010 | ||

| (0.0047) | |||

| SOE15 | 0.0048 | ||

| (0.0045) | |||

| Size | 0.0108** | 0.0106** | 0.0109*** |

| (0.0042) | (0.0042) | (0.0042) | |

| ROA | 0.6331*** | 0.6325*** | 0.6327*** |

| (0.0316) | (0.0316) | (0.0316) | |

| Cash | 0.0070*** | 0.0071*** | 0.0070*** |

| (0.0024) | (0.0024) | (0.0024) | |

| Leverage | –0.0260* | –0.0259* | –0.0257* |

| (0.0152) | (0.0152) | (0.0152) | |

| Growth | 0.0221*** | 0.0220*** | 0.0221*** |

| (0.0027) | (0.0027) | (0.0027) | |

| Bsize | –0.0184*** | –0.0182*** | –0.0184*** |

| (0.0060) | (0.0060) | (0.0060) | |

| Indb | –0.0065 | –0.0075 | –0.0078 |

| (0.0305) | (0.0305) | (0.0305) | |

| Largest | 0.0587*** | 0.0588*** | 0.0578*** |

| (0.0190) | (0.0190) | (0.0190) | |

| Dual | 0.0064* | 0.0063* | 0.0063* |

| (0.0034) | (0.0034) | (0.0034) | |

| Meeting | –0.0054* | –0.0056* | –0.0055* |

| (0.0032) | (0.0032) | (0.0032) | |

| Big4 | 0.0023 | 0.0023 | 0.0023 |

| (0.0094) | (0.0094) | (0.0094) | |

| Firm FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Constant | 0.3148*** | 0.3170*** | 0.3132*** |

| (0.0720) | (0.0719) | (0.0718) | |

| N | 20,564 | 20,564 | 20,564 |

| Adj. R2 | 0.1361 | 0.1359 | 0.1360 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively. SOE, state-owned enterprise; SOE13, a dummy variable indicating the implementation of the anti-corruption campaign affecting SOEs, established for the year 2013; SOE14, a dummy variable indicating the implementation of the policy prohibiting government officials from serving as independent directors in SOEs, established for the year 2014; SOE15, a dummy variable indicating the implementation of the classified promotion of mixed-ownership reform for SOEs, established for the year 2015.

In addition, we conduct other robustness tests as follows. First, to avoid the enhancement effect of the party organization governance on internal control quality being driven by differences between the treatment group and control group firms, we apply a propensity score matching approach to mitigate the model dependence of our causal effect estimators (Zhu et al., 2023). We first employ three matching methods (one-to-one nearest neighbor matching without replacement, caliper matching (neighbor (1) without replacement with a caliper range of 0.001), and kernel matching) to find similar treatment group firms to comparable control group firms. We then estimate model (1) using the matched samples. Appendix Table 8 shows the results of propensity score matching differences-in-differences (PSM-DID). The coefficients of Party remain positive and statistically significant, implying that party organization governance helps improve SOEs’ internal control quality.

Second, we change the indicators used to measure corporate internal control quality to ensure the robustness of the results. In particular, we refer to Li et al. (2021) and Liu et al. (2022) to measure corporate internal control quality using the natural logarithm of the DIB internal control index score plus one (LnIC) and the DIB internal control index score adjusted by the industry annual median divided by 1000 (ICadj). Moreover, we introduce one-period lead (t + 1) and two-period lead (t + 2) internal control quality data as dependent variables to mitigate endogeneity arising from potential reverse causation (Yuan et al., 2023). The results in columns (1)–(4) of Appendix Table 9 reveal that party organization governance still significantly improves internal control quality after changing the measures of internal control quality.

Third, the timing of implementing the CPOPD decision-making mechanism varies across firms. We perform Bacon decomposition following Goodman-Bacon (2021). Appendix Table 10 reports the coefficients and weights of each group. According to Appendix Table 10, the positive effect of party organization governance on internal control quality mainly stems from the treatment group and the control group that have never been treated, confirming the robustness of the research results. In addition, we assume that central SOEs implement the CPOPD decision-making mechanism in 2015 and that of local SOEs in 2016, and construct a policy dummy variable (PartyD1). Furthermore, as the notice for local SOEs was issued in October 2016, we construct another policy dummy variable (PartyD2) for the CPOPD decision-making mechanism implemented by central SOEs in 2015 and local SOEs in 2017. Appendix Table 11 shows that after assuming all SOEs implement the CPOPD decision-making mechanism, party organization governance significantly improves the quality of internal control.

Finally, to avoid the potential heterogeneity of SOEs affecting the results, we divide them into central and local SOEs, as well as regulated and market-oriented SOEs. The classification standards for regulated and market-oriented SOEs are not universally defined. Regulated SOEs are usually related to national security and the lifeline of the national economy, where the degree of market competition is relatively low. Market-oriented SOEs are operating in fully competitive markets. Thus, we classify SOEs as regulated and market-oriented based on the annual median of HHI. Appendix Table 12 reports the estimated results. The central SOEs are the treatment group in columns (1) and (2), the control group is local SOEs and non-SOEs in column (1), and only non-SOEs in column (2). The local SOEs are the treatment group in columns (3) and (4), the control group is central SOEs and non-SOEs in column (3), and only non-SOEs in column (4). Columns (5) and (6) represent the market-oriented and regulated SOEs. Appendix Table 12 reveals that party organization governance improves the internal control quality of SOEs in the sub-sample tests.

The previous theoretical analysis indicates that party organization governance formed by the CPOPD decision-making mechanism may enhance internal control quality by reducing corporate violations, inhibiting earnings manipulation, and curbing on-the-job consumption. Following Baron and Kenny (1986) and Chen et al. (2022), we construct models (3) and (4) to test how party organization governance affects internal control quality.

Mechanism contains three variables: corporate violations (CV), earnings manipulation (EM), and on-the-job consumption ratio (CR). Specifically, we adopt the number of violations per year for each firm to measure corporate violations (CV). We use discretionary accruals to measure earnings manipulation (EM). EM is calculated using a cross-sectional version of the modified Jones (1991) model, which has been widely used in the literature on earnings manipulation (Han et al., 2022). We then compute the percentage of total on-the-job consumption relative to operating revenue to measure on-the-job consumption (CR). On-the-job consumption includes administrative expenses, travel charges, business entertainment, communication expenses, training expenses, convention expenses, and car fare (Cai et al., 2011). All other variables are consistent with model (1).

The results are shown in Table 6. The coefficient of Party in column (1) is significantly negative at the 1% level, indicating that party organization governance reduces corporate violations. The coefficient of CV in column (2) is significantly negative, indicating that corporate violations are negatively related to internal control quality. The Sobel test result shows that corporate violations mediate the relationship between party organization governance and internal control quality (Z = 6.225, p-value = 0.000).

| (1) | (2) | (3) | (4) | (5) | (6) | |

| CV | IC | EM | IC | CR | IC | |

| Party | –0.0961*** | 0.0109*** | –0.1972*** | 0.0130*** | –0.0810*** | 0.0137*** |

| (0.0166) | (0.0036) | (0.0466) | (0.0037) | (0.0217) | (0.0037) | |

| CV | –0.0331*** | |||||

| (0.0023) | ||||||

| EM | –0.0055*** | |||||

| (0.0008) | ||||||

| CR | –0.0046* | |||||

| (0.0026) | ||||||

| Size | –0.0315* | 0.0095** | 0.1056** | 0.0111*** | –0.1295*** | 0.0099** |

| (0.0171) | (0.0041) | (0.0471) | (0.0042) | (0.0281) | (0.0042) | |

| ROA | –0.6525*** | 0.6110*** | –0.8121*** | 0.6281*** | –1.5651*** | 0.6253*** |

| (0.1241) | (0.0307) | (0.3109) | (0.0313) | (0.1638) | (0.0319) | |

| Cash | –0.0143 | 0.0067*** | –0.2329*** | 0.0059** | –0.0009 | 0.0072*** |

| (0.0108) | (0.0024) | (0.0260) | (0.0024) | (0.0128) | (0.0024) | |

| Leverage | 0.2803*** | –0.0166 | 1.1556*** | –0.0195 | –0.1091 | –0.0264* |

| (0.0587) | (0.0148) | (0.1548) | (0.0152) | (0.0981) | (0.0152) | |

| Growth | –0.0342*** | 0.0209*** | 0.1860*** | 0.0230*** | –0.1799*** | 0.0212*** |

| (0.0121) | (0.0026) | (0.0386) | (0.0027) | (0.0166) | (0.0028) | |

| Bsize | 0.0410 | –0.0164*** | 0.0955 | –0.0173*** | 0.0232 | –0.0177*** |

| (0.0263) | (0.0058) | (0.0647) | (0.0059) | (0.0280) | (0.0059) | |

| Indb | –0.1654** | 0.0534*** | –0.4702* | 0.0563*** | –0.2946** | 0.0575*** |

| (0.0743) | (0.0186) | (0.2459) | (0.0189) | (0.1253) | (0.0189) | |

| Largest | 0.0193 | 0.0068** | –0.0204 | 0.0061* | 0.0246 | 0.0063* |

| (0.0170) | (0.0033) | (0.0397) | (0.0033) | (0.0224) | (0.0034) | |

| Dual | 0.1249*** | –0.0015 | –0.0252 | –0.0058* | 0.0578*** | –0.0054* |

| (0.0162) | (0.0031) | (0.0374) | (0.0032) | (0.0198) | (0.0032) | |

| Meeting | –0.0603** | 0.0003 | –0.0667 | 0.0019 | –0.0157 | 0.0022 |

| (0.0303) | (0.0093) | (0.0972) | (0.0095) | (0.0414) | (0.0094) | |

| Big4 | –0.0315* | 0.0095** | 0.1056** | 0.0111*** | –0.1295*** | 0.0099** |

| (0.0171) | (0.0041) | (0.0471) | (0.0042) | (0.0281) | (0.0042) | |

| Sobel Z | 6.225 | 4.700 | 2.522 | |||

| p-value | 0.000 | 0.000 | 0.012 | |||

| Firm FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 0.6835** | 0.3365*** | 3.9932*** | 0.3358*** | 3.7625*** | 0.3312*** |

| (0.2784) | (0.0687) | (0.8313) | (0.0700) | (0.5415) | (0.0708) | |

| N | 20,564 | 20,564 | 20,564 | 20,564 | 20,564 | 20,564 |

| Adj. R2 | 0.0290 | 0.1575 | 0.2388 | 0.1392 | 0.0870 | 0.1363 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively. CV, corporate violations; EM, earnings manipulation; CR, the on-the-job consumption ratio.

In column (3), the coefficient of Party is significantly negative, suggesting that party organization governance inhibits earnings manipulation. The coefficient of EM in column (4) is significantly negative at the 1% level, suggesting that earnings manipulation is negatively associated with internal control quality. We employ the Sobel test for further confirmation. The result of the Sobel test indicates that earnings manipulation plays a mediating role in the relationship between party organization governance and internal control quality (Z = 4.700, p-value = 0.000).

The coefficient of Party is statistically significantly negative in column (5), showing that party organization governance restrains on-the-job consumption of executives. The coefficient of CR in column (6) is significantly negative, indicating that executives’ on-the-job consumption is negatively related to internal control quality. After conducting the Sobel test, we find that on-the-job consumption plays a significant mediating role in the relationship between party organization governance and internal control quality (Z = 2.522, p-value = 0.012).

The results in Tables 3,6 demonstrate that reducing corporate violations, inhibiting earnings manipulation, and curbing on-the-job consumption are the main channels through which party organization governance improves the quality of internal control.

Following the theoretical analysis in the previous section, we perform a heterogeneity analysis on firms with different executive shareholdings and different analyst attention to test Hypotheses 2 and 3.

We divide the sample into firms with more executive shareholding (ESM Group) and firms with lower executive shareholding (ESL Group) according to the median executive shareholding and perform a subsample analysis based on model (1). The results are displayed in columns (1) and (2) of Table 7. The coefficient of Party in column (1) is insignificant, while the coefficient in column (2) is significant at the 5% level. Party organization governance has an insignificant impact on internal control quality in firms with more executive shareholding but a significant positive effect on internal control quality in firms with lower executive shareholding. These results indicate that party organization governance plays a more significant role in improving internal control quality in firms with lower executive shareholding than in firms with more executive shareholding. Hypothesis H2 is supported.

| ESM Group | ESL Group | AAM Group | AAL Group | |

| (1) | (2) | (3) | (4) | |

| IC | IC | IC | IC | |

| Party | 0.0032 | 0.0146** | 0.0020 | 0.0251*** |

| (0.0062) | (0.0061) | (0.0047) | (0.0061) | |

| Size | 0.0032 | 0.0146** | 0.0031 | 0.0179*** |

| (0.0062) | (0.0061) | (0.0057) | (0.0051) | |

| ROA | 0.0042 | 0.0161** | 0.0030 | 0.0119* |

| (0.0055) | (0.0067) | (0.0059) | (0.0062) | |

| Cash | 0.5705*** | 0.6635*** | 0.6870*** | 0.5548*** |

| (0.0404) | (0.0529) | (0.0419) | (0.0497) | |

| Leverage | 0.0100*** | 0.0047 | 0.0114*** | 0.0048 |

| (0.0033) | (0.0036) | (0.0034) | (0.0035) | |

| Growth | 0.0021 | –0.0508** | –0.0144 | –0.0298 |

| (0.0187) | (0.0248) | (0.0181) | (0.0231) | |

| Bsize | 0.0234*** | 0.0246*** | 0.0208*** | 0.0235*** |

| (0.0036) | (0.0039) | (0.0035) | (0.0044) | |

| Indb | –0.0093 | –0.0257*** | –0.0118 | –0.0297*** |

| (0.0070) | (0.0091) | (0.0080) | (0.0092) | |

| Largest | 0.0531* | 0.0478* | 0.0396 | 0.0916*** |

| (0.0289) | (0.0274) | (0.0254) | (0.0303) | |

| Dual | 0.0077* | 0.0088 | 0.0006 | 0.0095* |

| (0.0042) | (0.0061) | (0.0050) | (0.0050) | |

| Meeting | –0.0092** | –0.0042 | –0.0025 | –0.0057 |

| (0.0039) | (0.0054) | (0.0044) | (0.0048) | |

| Big4 | 0.0146 | –0.0095 | 0.0139 | –0.0057 |

| (0.0102) | (0.0140) | (0.0117) | (0.0120) | |

| Constant | 0.3889*** | 0.2573** | 0.3777*** | 0.3460*** |

| (0.0945) | (0.1147) | (0.0964) | (0.1096) | |

| N | 10,282 | 10,282 | 10,441 | 10,296 |

| Adj. R2 | 0.1632 | 0.1156 | 0.1639 | 0.1066 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively. ESM and ESL refer to firms with more executive shareholding and firms with lower executive shareholding, respectively. AAM and AAL refer to firms with more analyst attention and firms with lower analyst attention, respectively.

We use the natural logarithm of the number of analysts covering the firm in the current year plus one to measure analyst attention following Zhou et al. (2024). Based on the median of analyst attention, we classify the sample firms into firms with more analyst attention (AAM Group) and firms with lower analyst attention (AAL Group). Columns (3) and (4) of Table 7 demonstrate the heterogeneity of the results by analyst attention level. The estimated coefficient of Party is insignificant in column (3), but significantly positive in column (4), suggesting that party organization governance has an insignificant effect on internal control quality in firms with more analyst attention, but significantly promotes internal control quality in firms with lower analyst attention (Hypothesis H3 is confirmed). This pattern can be explained by the fact that analyst attention has a stronger external governance role in firms with more analyst attention, diminishing the role of party organization governance in such firms. However, firms with lower analyst attention lack a robust external governance mechanism. Party organization governance can effectively compensate for the deficiency of external supervision, improve and strengthen the internal supervision system, and thus improve internal control quality.

In the context of the Chinese government’s emphasis on establishing a healthy internal control system for SOEs, we exploit the implementation of the CPOPD decision-making mechanism as an opportunity to examine the impact of party organization governance on internal control quality. We adopt a sample of A-share listed firms in Shanghai and Shenzhen from 2012 to 2022 and employ a difference-in-differences method to examine the impact and mechanism of party organization governance formed by the CPOPD decision-making mechanism in SOEs on internal control quality. We find that party organization governance significantly improves SOEs’ internal control quality. Furthermore, party organization governance improves internal control quality by reducing corporate violations, inhibiting earnings manipulation, and curbing on-the-job consumption. Party organization governance significantly enhances internal control quality in firms with lower executive shareholding but has an insignificant effect on internal control quality in firms with more executive shareholding. In addition, the positive effect of party organization governance on internal control quality is more pronounced in firms with lower analyst attention than in firms with more analyst attention.

This study provides several important theoretical implications. First, existing literature predominantly examines the economic effects of party organization governance formed by the overlap between party members and management in SOEs (Li et al., 2020; Wang et al., 2023). Few studies investigate the impact of party organization governance formed by the CPOPD decision-making mechanism on corporate governance and corporate value (Xie et al., 2022; Wang et al., 2025). However, little research explores the relationship between party organization governance formed by the CPOPD decision-making mechanism and internal control quality. We define party organization governance by whether firms amended their articles of association to implement the CPOPD decision-making mechanism and reveal the impact of party organization governance on internal control quality from both theoretical and empirical perspectives. Our research supplements the relevant literature on party organization governance and internal control quality.

Second, existing literature primarily reveals the channels through which corporate governance affects internal control quality from agency theory perspective (Li et al., 2021; Han et al., 2022). The CPOPD decision-making mechanism, as a formal institutional arrangement stipulating party organizations’ participation in SOE governance, establishes the legitimacy of party organization governance (Lin and Milhaupt, 2021). Therefore, we integrate institutional theory and agency theory to clarify the underlying mechanisms through which party organization governance affects internal control quality, illuminating the unique role of party organization governance within Chinese political institutions from institutional foundations and implementation routes.

Finally, traditional corporate governance theory, grounded in Western market environments, emphasizes internal incentives and external supervision as core mechanisms for mitigating agency conflicts and thereby enhancing internal control quality. We investigate the heterogeneous effects of party organization governance on internal control quality across different executive shareholdings (internal incentives) and different analyst attention (external supervision) within China’s unique governance system. Our findings indicate that party organization governance effectively supplements deficient internal incentives and external supervision, broadening the theoretical understanding of governance mechanism diversity within the Chinese context.

Our findings have several practical implications. First, party organization governance significantly optimizes internal control quality. Thus, the Chinese government should continue to promote and implement the CPOPD decision-making mechanism in SOEs. Lin and Milhaupt (2021) point out that the CPOPD decision-making mechanism in some SOEs is symbolic rather than substantively enforced, and the adoption rate of party organization opinions is relatively low. For example, Sichuan Provincial Investment Group Co., Ltd. failed to implement the CPOPD decision-making mechanism, resulting in inadequate supervision of major decision-making matters and a weak internal control system. The deputy general manager of the company made illegal decisions that caused huge losses to state-owned assets. Accordingly, the Chinese government should establish and evaluate specific implementation indicators for the CPOPD decision-making mechanism, such as the proportion of matters pre-discussed by party organizations and the adoption rate of party organization opinions. For SOEs with low core indicators, regulatory departments should promptly mandate rectification. Additionally, boards should alter their perception of party organization governance, recognizing that party organization participation in governance is not merely a compliance requirement, but a pivotal mechanism for enhancing internal control effectiveness, and actively facilitate the implementation of the CPOPD decision-making mechanism.

Second, the Chinese government should formulate a detailed checklist of pre-discussion items, clarify the rights and responsibilities of the party organization and management in major matters, weaken the discretionary power of executives over major matters, and reduce corporate violations, earnings manipulation, and on-the-job consumption at the source. For instance, China Nuclear Engineering lacks a clear list of pre-discussion items, resulting in ineffective implementation of the CPOPD decision-making mechanism. The proportion of expenses such as business entertainment expenses, business vehicle purchase and operation, and maintenance expenses is relatively high, with many violations. Therefore, it is crucial to formulate a detailed and enforceable pre-discussion checklist to ensure effective policy execution. Further, boards should design quantifiable indicators to regularly assess the contribution of party organizations to internal control quality through pre-discussion of “Three Major and One Large” matters. These assessment results guide adjustments to party organizations’ participation in major decision-making, such as optimizing the pre-discussion checklist.

Finally, the Chinese government should promote and improve the CPOPD decision-making mechanism based on the actual circumstances of different firms. On the one hand, for firms with lower executive shareholding, it is advisable to consider integrating internal control quality with executive compensation to incentivize executives to improve internal control quality. On the other hand, for firms with lower analyst attention, it is necessary to strengthen special reports on internal control quality and increase incentives to attract external analyst attention. Combining internal and external governance mechanisms can effectively improve internal control quality in SOEs.

The data that support the findings of this study are available from the corresponding author upon reasonable request.

ST designed the research study. ST and SW performed data collection and analysis for the study. SW provided help and advice on the research study. Both authors contributed to critical revision of the manuscript for important intellectual content. Both authors read and approved the final manuscript. Both authors have participated sufficiently in the work and agreed to be accountable for all aspects of the work.

Not applicable.

Improving Scientific Research Basic Ability of Young and Middle-aged Teachers in Guangxi Universities (2025KY0008).

The authors declare no conflict of interest.

See Fig. 3 and Tables 8,9,10,11,12.

Fig. 3.

Fig. 3. The IC in the treatment and control groups.

| Nearest-neighbor matching | Caliper matching | Kernel matching | |

| (1) | (2) | (3) | |

| IC | IC | IC | |

| Party | 0.0131*** | 0.0119** | 0.0142*** |

| (0.0038) | (0.0047) | (0.0037) | |

| Size | 0.0122*** | 0.0045 | 0.0108** |

| (0.0046) | (0.0058) | (0.0042) | |

| ROA | 0.5765*** | 0.6979*** | 0.6314*** |

| (0.0336) | (0.0461) | (0.0316) | |

| Cash | 0.0058** | 0.0104*** | 0.0070*** |

| (0.0026) | (0.0032) | (0.0024) | |

| Leverage | –0.0406** | –0.0076 | –0.0261* |

| (0.0162) | (0.0192) | (0.0152) | |

| Growth | 0.0213*** | 0.0245*** | 0.0230*** |

| (0.0029) | (0.0037) | (0.0027) | |

| Bsize | –0.0220*** | –0.0163** | –0.0185*** |

| (0.0066) | (0.0080) | (0.0060) | |

| Indb | –0.0242 | 0.0578 | –0.0115 |

| (0.0311) | (0.0432) | (0.0308) | |

| Largest | 0.0575*** | 0.0478** | 0.0563*** |

| (0.0211) | (0.0230) | (0.0185) | |

| Dual | 0.0054 | –0.0009 | 0.0062* |

| (0.0035) | (0.0046) | (0.0033) | |

| Meeting | –0.0041 | –0.0053 | –0.0054* |

| (0.0034) | (0.0042) | (0.0032) | |

| Big4 | 0.0028 | 0.0120 | 0.0023 |

| (0.0110) | (0.0135) | (0.0094) | |

| Firm FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Constant | 0.3278*** | 0.3492*** | 0.3188*** |

| (0.0799) | (0.1009) | (0.0726) | |

| N | 17,892 | 11,965 | 20,433 |

| Adj. R2 | 0.1197 | 0.1390 | 0.1364 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively.

| (1) | (2) | (3) | (4) | |

| LnIC | ICadj | IC(t + 1) | IC(t + 2) | |

| Party | 0.1190*** | 0.0142*** | 0.0188*** | 0.0163*** |

| (0.0312) | (0.0037) | (0.0036) | (0.0044) | |

| Size | 0.0902** | 0.0112*** | –0.0258*** | –0.0332*** |

| (0.0383) | (0.0042) | (0.0047) | (0.0057) | |

| ROA | 4.0631*** | 0.6242*** | 0.2767*** | 0.2378*** |

| (0.3142) | (0.0314) | (0.0312) | (0.0365) | |

| Cash | 0.0348 | 0.0065*** | 0.0102*** | 0.0116*** |

| (0.0221) | (0.0024) | (0.0024) | (0.0027) | |

| Leverage | –0.3178** | –0.0268* | –0.0050 | –0.0223 |

| (0.1378) | (0.0153) | (0.0151) | (0.0183) | |

| Growth | 0.0031 | 0.0214*** | 0.0083*** | 0.0009 |

| (0.0244) | (0.0027) | (0.0030) | (0.0030) | |

| Bsize | –0.1643*** | –0.0179*** | –0.0138** | –0.0004 |

| (0.0568) | (0.0060) | (0.0060) | (0.0064) | |

| Indb | –0.1393 | –0.0045 | –0.0705** | –0.0258 |

| (0.2606) | (0.0305) | (0.0290) | (0.0367) | |

| Largest | 0.3863** | 0.0596*** | 0.0692*** | 0.0830*** |

| (0.1669) | (0.0191) | (0.0204) | (0.0267) | |

| Dual | 0.0684** | 0.0059* | 0.0031 | 0.0075* |

| (0.0290) | (0.0034) | (0.0037) | (0.0043) | |

| Meeting | –0.0545** | –0.0061* | –0.0028 | –0.0072* |

| (0.0274) | (0.0032) | (0.0036) | (0.0039) | |

| Big4 | –0.0275 | 0.0033 | 0.0195 | 0.0208 |

| (0.0700) | (0.0094) | (0.0122) | (0.0136) | |

| Firm FE | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes |

| Constant | 4.1110*** | –0.3818*** | 1.0436*** | 1.1324*** |

| (0.6536) | (0.0721) | (0.0851) | (0.1108) | |

| N | 20,564 | 20,564 | 17,039 | 15,711 |

| Adj. R2 | 0.0647 | 0.1141 | 0.0442 | 0.0335 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively.

| Differences-in-Differences (DID) Comparison | Weight | Avg DID Est |

| Earlier Treatment vs. Later Comparison | 0.069 | 0.011 |

| Later Treatment vs. Earlier Comparison | 0.044 | –0.008 |

| Treatment vs. Never treated | 0.886 | 0.028 |

| Treatment vs. Already treated | 0.001 | –0.001 |

| (1) | (2) | |

| IC | IC | |

| PartyD1 | 0.0097*** | |

| (0.0037) | ||

| PartyD2 | 0.0090** | |

| (0.0036) | ||

| Size | 0.0105** | 0.0102** |

| (0.0042) | (0.0042) | |

| ROA | 0.6341*** | 0.6334*** |

| (0.0315) | (0.0315) | |

| Cash | 0.0072*** | 0.0073*** |

| (0.0024) | (0.0024) | |

| Leverage | –0.0273* | –0.0272* |

| (0.0153) | (0.0153) | |

| Growth | 0.0223*** | 0.0222*** |

| (0.0027) | (0.0027) | |

| Bsize | –0.0184*** | –0.0184*** |

| (0.0060) | (0.0060) | |

| Indb | –0.0068 | –0.0066 |

| (0.0305) | (0.0305) | |

| Largest | 0.0622*** | 0.0623*** |

| (0.0191) | (0.0191) | |

| Dual | 0.0064* | 0.0064* |

| (0.0034) | (0.0034) | |

| Meeting | –0.0049 | –0.0052 |

| (0.0032) | (0.0032) | |

| Big4 | 0.0021 | 0.0020 |

| (0.0095) | (0.0095) | |

| Firm FE | Yes | Yes |

| Year FE | Yes | Yes |

| Constant | 0.3146*** | 0.3200*** |

| (0.0719) | (0.0719) | |

| N | 20,564 | 20,564 |

| Adj. R2 | 0.1354 | 0.1354 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively.

| (1) | (2) | (3) | (4) | (5) | (6) | |

| IC | IC | IC | IC | IC | IC | |

| Party | 0.0146*** | 0.0181*** | 0.0085** | 0.0154*** | 0.0099* | 0.0167*** |

| (0.0056) | (0.0059) | (0.0040) | (0.0042) | (0.0056) | (0.0051) | |

| Size | 0.0096** | 0.0046 | 0.0099** | 0.0130*** | 0.0198*** | 0.0060 |

| (0.0042) | (0.0049) | (0.0042) | (0.0046) | (0.0070) | (0.0052) | |

| ROA | 0.6337*** | 0.6452*** | 0.6342*** | 0.5839*** | 0.5822*** | 0.6574*** |

| (0.0315) | (0.0361) | (0.0316) | (0.0315) | (0.0568) | (0.0379) | |

| Cash | 0.0076*** | 0.0086*** | 0.0075*** | 0.0071*** | –0.0002 | 0.0105*** |

| (0.0024) | (0.0028) | (0.0024) | (0.0026) | (0.0040) | (0.0029) | |

| Leverage | –0.0270* | –0.0126 | –0.0277* | –0.0257 | –0.0826*** | 0.0009 |

| (0.0152) | (0.0181) | (0.0152) | (0.0157) | (0.0244) | (0.0188) | |

| Growth | 0.0221*** | 0.0215*** | 0.0222*** | 0.0235*** | 0.0226*** | 0.0222*** |

| (0.0027) | (0.0031) | (0.0027) | (0.0029) | (0.0039) | (0.0036) | |

| Bsize | –0.0181*** | –0.0212*** | –0.0180*** | –0.0134** | –0.0188** | –0.0180** |

| (0.0060) | (0.0076) | (0.0060) | (0.0063) | (0.0093) | (0.0078) | |

| Indb | –0.0053 | –0.0187 | –0.0067 | –0.0136 | –0.0452 | 0.0119 |

| (0.0305) | (0.0400) | (0.0305) | (0.0322) | (0.0515) | (0.0377) | |

| Largest | 0.0642*** | 0.0698*** | 0.0639*** | 0.0526** | 0.0149 | 0.0741*** |

| (0.0189) | (0.0240) | (0.0191) | (0.0207) | (0.0322) | (0.0232) | |

| Dual | 0.0061* | 0.0063 | 0.0062* | 0.0070** | 0.0083 | 0.0051 |

| (0.0034) | (0.0040) | (0.0034) | (0.0035) | (0.0055) | (0.0042) | |

| Meeting | –0.0051 | –0.0076** | –0.0050 | –0.0072** | –0.0002 | –0.0086** |

| (0.0032) | (0.0038) | (0.0032) | (0.0034) | (0.0052) | (0.0040) | |

| Big4 | 0.0018 | –0.0004 | 0.0025 | 0.0149 | –0.0142 | 0.0120 |

| 0.0096** | 0.0046 | 0.0099** | 0.0130*** | 0.0198*** | 0.0060 | |

| Firm FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 0.3261*** | 0.4253*** | 0.3222*** | 0.2665*** | 0.3117*** | 0.3315*** |

| (0.0719) | (0.0825) | (0.0721) | (0.0772) | (0.1203) | (0.0889) | |

| N | 20,564 | 14,299 | 20,564 | 17,313 | 7269 | 13,295 |

| Adj. R2 | 0.1355 | 0.1512 | 0.1353 | 0.1388 | 0.1319 | 0.1397 |

Notes: Standard errors are clustered at the firm level and appear in parentheses. *, **, and *** indicate significance levels at 10%, 5%, and 1%, respectively.

References

Publisher’s Note: IMR Press stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.