, Kamran Ali 1,2,*

, Kamran Ali 1,2,* , Muhammad Siddique Malik 2, Muhammad Haroon Rasheed 1,3, Wasim ul Rehman 4

, Muhammad Siddique Malik 2, Muhammad Haroon Rasheed 1,3, Wasim ul Rehman 41 College of Economics and Management, Nanjing University of Aeronautics and Astronautics, 210016 Nanjing, Jiangsu, China

2 Department of Commerce, University of the Punjab, Gujranwala Campus, 52210 Gujranwala, Pakistan

3 Malik Firoz Khan Noon Business School, University of Sargodha, 40100 Sargodha, Pakistan

4 Department of Business Administration, University of the Punjab, Gujranwala Campus, 52210 Gujranwala, Pakistan

Abstract

This study investigates the mediating role of green innovation in the relationship between green practices (e.g., environmental management accounting, green intellectual capital, and environmental ethics) and environmental performance, drawing on the Natural Resource-Based View (NRBV). Moreover, it examines the moderating effect of managerial environmental concern (MEC) on the relationship between green innovation and environmental performance. Survey data were collected from 397 finance managers and management accountants working in ISO 14000-certified manufacturing companies. Smart PLS 4 was employed to analyze the proposed research model. The results demonstrate a significant positive relationship between green practices and environmental performance, both directly and indirectly through green innovation. Moreover, managerial environmental concern significantly moderates the relationship between green innovation and environmental performance. This study extends the NRBV by being the first study in Pakistan’s manufacturing sector to theorize and test how green practices improve environmental performance through green innovation as a mediator and how MEC moderates this relationship. The findings offer new theoretical insights for sustainability in resource-constrained economies and provide practical implications for managers and policymakers in Pakistan.

Keywords

- green intellectual capital

- innovation

- environmental management accounting

- environmental ethics

- environmental performance

Environmental sustainability has emerged as a critical global priority, particularly in light of rising concerns over climate change, resource depletion, and ecological degradation (Aftab et al, 2022). Although the manufacturing industry provides employment opportunities and plays a significant role in global economic growth, it is also responsible for global warming through the emission of greenhouse gases, which cause environmental imbalances (Aftab et al, 2022). This dual role of the industrial sector is a critical challenge (Jahanger et al, 2022). Consequently, environmental concerns have grown at an alarming rate, compelling firms to embrace sustainable manufacturing processes.

The accelerated industrialization observed over the past two decades has heightened environmental issues, such as deforestation, water pollution, and global warming (Aftab et al, 2022). Organizations are therefore experiencing tremendous pressure to achieve a balance between economic growth and environmental sustainability (Babiak and Trendafilova, 2011; Brown and Dillard, 2014; Wu and Pagell, 2011). In response, organizations are increasingly allocating resources toward the adoption of sustainable production techniques, including the implementation of advanced management systems, the development of eco-innovations, and the integration of stakeholder perspectives (Munodawafa and Johl, 2019; Tamayo-Orbegozo et al, 2017). These green approaches facilitate sustainable economic processes while mitigating environmental impacts (Wong et al, 2012).

Among these approaches, green intellectual capital (GIC) has emerged as a crucial resource that connects external knowledge with internal incentives, facilitating the alignment of organizational interactions with the natural environment (Begum et al, 2023; Bombiak, 2022; Shoukat et al, 2024). While green innovation is widely recognized as a driver of environmental performance (Fang et al, 2021; Zheng et al, 2023), GIC (See Appendix Table 6 for definitions) in the context of green innovation (GI) as a mediator remains underexplored. Furthermore, the proficiency of the workforce is essential for sustainability, as an organization cannot adopt a green philosophy without aligning its intellectual capital with environmental objectives.

Environmental management accounting (EMA) serves as a strategic instrument that enables organizations to identify and report environmental costs, thereby enhancing data-driven decision-making related to environmental management. GIC encompasses the organization’s intangible resources, including employee competencies, structural systems, and stakeholder networks, which facilitate innovation in accordance with ecological objectives. Environmental ethics (ENETH) plays a crucial role in shaping the ethical orientation of organizational culture, thereby influencing pro-environmental behaviors and fostering a long-term commitment to sustainability. When combined, these constructs establish a synergistic framework of green practices rooted in the Natural Resource-Based View (NRBV), which asserts that internal competencies and values can be strategically leveraged to achieve both environmental and competitive advantages. This integration enhances firms’ capacity to develop, adopt, and sustain GI, which is widely recognized as a mediator between internal practices and environmental outcomes (Fang et al, 2021; Zheng et al, 2023). However, previous research has predominantly examined these constructs in isolation; this study therefore contributes to the literature by exploring their synergistic effects on environmental performance and the interactions facilitated by GI. Furthermore, this study incorporates managerial environmental concern (MEC) as a contextual moderator, representing an organization’s capacity to implement techniques and processes that mitigate adverse environmental effects, while also making a positive contribution to the literature. Support from management is essential for the successful implementation of green innovation projects as it enhances environmental performance by providing clear guidance and assistance (Zhang et al, 2020). However, the interaction between these factors in driving environmental performance (ENP), in the context of green innovation, remains an open research area.

This research aims to address these gaps by investigating the effects of EMA, GIC, and ENETH on environmental performance, as well as the mediating role of green innovation and the moderating role of MEC on GI and ENP. In order to address the research objectives and test the hypotheses, this study employed Partial Least Squares Structural Equation Modeling (PLS-SEM). Pakistan was chosen for a number of compelling reasons. Firstly, the country has established itself as an increasingly significant participant in global manufacturing value chains, particularly in the sectors of textiles, leather, and food processing, which are closely interconnected with international buyers. Secondly, industrial firms are progressively implementing sustainability practices in response to regulatory and market pressures. Thirdly, the environmental vulnerabilities of Pakistan—aggravated by swift industrialization—render it a vital context for examining the relationship between green innovation and environmental performance. For example, the country has witnessed unprecedented climate events (e.g., the 2022 floods), which have intensified calls for corporate environmental responsibility. Finally, several initiatives, such as the “Green Industrial Policy” and alignment with the Sustainable Development Goals (SDGs), underscore a national momentum toward sustainable manufacturing, thereby establishing Pakistan as a relevant and timely context for this study (El Khatib et al, 2020).

The remaining part of the research is structured as follows: The theoretical foundation, literature review, and hypotheses are covered in Section 2. The methodology and analytical tools are presented in Section 3 with data analysis and results in Section 4, while discussion on hypotheses are included in Section 5. Conclusion in section 6. Theoretical and practical implications in section 7 and Limitations and future research directions in section 8.

This study adheres to NRBV theory, which recognizes the importance of environmental care in developing organizational strategies and decision-making processes (Begum et al, 2023). NRBV has evolved into an important concept in strategic management because it underlines an organization’s ability to cultivate capabilities and resources to effectively utilize natural resources. NRBV theory focuses on the natural environment, urging firms to strengthen their skills and build systems aimed at minimizing pollution and waste while supporting eco-friendly industrial practices to improve overall performance (Amores-Salvadó et al, 2014; Rehman et al, 2021).

Rehman et al (2021) advanced NRBV by proposing that GIC is both an implicit resource and an energetic skill competence that allows enterprises to create pro-environmental strategies. From this perspective, firms that increase the influence of GIC on GI and, eventually, ENP, can gain a competitive edge. Furthermore, NRBV promotes environmental ethics and legislation, encouraging a proactive approach to strategic planning (Suki et al, 2022). This study contends that GIC, as a strategic means, helps enterprises capture green knowledge, environmental accounting, and environmental ethics, thereby enabling NRBV to produce green innovations and strategies aimed at restoring the planet.

The NRBV theory emphasizes that firms gain a sustainable competitive advantage by cultivating valuable and unique environmental resources and capabilities that enable them to reduce environmental costs and improve overall performance (Hart, 1995; Russo and Fouts, 1997). EMA closely aligns with this theoretical framework by enabling organizations to systematically monitor and manage their environmental impact while enhancing overall environmental performance. The adoption of EMA assists firms not only in fulfilling their environmental responsibilities but also in realizing financial benefits through improved environmental and economic performance (Khanam et al, 2023). EMA emphasizes the importance of environmental costs while providing insights into material flows, resulting in improvements in both economic and environmental performance (Mishra et al, 2022). Empirical evidence supports the positive role of EMA in driving environmental performance, as literature reveal that active engagement in EMA significantly enhances environmental performance (Aftab et al, 2023). Furthermore, studies in various contexts confirm the significant increase in environmental performance due to active EMA implementation (Appannan et al, 2023). Using the aforementioned reasoning and NRBV theory, the following hypothesis is proposed:

H1. There is a positive relationship between EMA and ENP.

NRBV highlights environmental ethics as a vital strategic resource that can influence firms’ environmental performance and support the creation of long-term competitive advantage (Bansal and Roth, 2000; Hart and Dowell, 2011). A company’s capacity to improve ENP through a value-driven strategy is fundamentally rooted in its internal resource of environmental ethics (Palmer et al, 2014). This performance depends on how successfully a company uses its resources in harmony with the environment, as well as its unwavering dedication to tight control over pollution emissions (Singh et al, 2019). Drawing on the NRBV, we argue that firms strategically leverage core resources, such as environmental ethics, to improve their ENP and achieve a competitive advantage. Moreover, corporate environmental ethics significantly shape a firm’s proactive environmental initiatives, thereby influencing its environmental performance. Such ethical orientations motivate organizations to integrate environmental management into their overall business philosophy, engaging all stakeholders in the pursuit of a greener enterprise (Guo et al, 2024). In line with the NRBV, this study proposes the following hypothesis:

H2. Environmental ethics positively influence environmental performance.

According to the NRBV, a firm’s competitive advantage largely depends on its core resources and capabilities, particularly those related to environmental management and sustainability (Hart, 1995; Russo and Fouts, 1997). Firms that embrace environmental responsibility can achieve a sustainable competitive advantage (Asiaei et al, 2022a). GIC comprising green human, structural and relational capital is defined as all intangible assets, such as knowledge, talents, and relationships, that support environmental preservation and innovation at both individual and organizational levels (Benevene et al, 2021).

Green human capital represents employees’ knowledge, skills, experience, attitudes, creativity, and dedication to acting environmentally (Chang, 2016). Green structural capital involves organizational capabilities, commitments, knowledge management systems, and processes that formalize environmental efforts (Chang and Chen, 2012). Green relational capital refers to external stakeholder relationships centered on shared environmental goals, enhancing value creation and competitive advantage (Hadj et al, 2020; Haldorai et al, 2022). Understanding the relevance of this green trend, companies attempt to obtain additional resources to strengthen their external ties with shared environmental goals, highlighting the value of green relational capital (Haldorai et al, 2022). This entails cultivating interaction ties with stakeholders regarding green innovation and corporate environmental management, leading to wealth creation and a competitive advantage (Hadj et al, 2020).

Together, GIC enhances a firm’s environmental reputation, reduces environmental costs, and promotes eco-friendly practices. As highlighted by Asiaei et al (2022a), the effective acquisition and deployment of green resources and knowledge are crucial for environmental success. Thus, we hypothesize:

H3. GIC (including green human capital, green structural capital, and green relational capital) positively influences ENP.

Green innovation allows firms to reduce waste, lower costs, and enhance the value of their goods and services. EMA catalyzes green innovation by providing the structural tools and data necessary to identify environmental impacts, monitor resource use, and uncover opportunities for improvement (Gomez-Conde et al, 2019). Through EMA, organizations gain complete insight into their environmental impact, which supports innovative problem-solving efforts. These innovations, fueled by EMA data and insights, change processes, goods, or habits that directly improve environmental performance (Benzidia et al, 2024). EMA-driven insights support GI by efficiently allocating resources to create environmentally friendly processes and products. By incorporating environmental issues into decision-making, EMA promotes strategic alignment across enterprises (Guenther et al, 2016).

EMA drives green innovation, which results in distinctive, eco-friendly services that, when adopted by the market, increase market share, revenue, and brand loyalty. This competitive advantage gained from green innovation improves environmental performance by encouraging eco-conscious corporate operations that attract environmentally aware customers (Buhl et al, 2016). These relationships demonstrate how EMA adoption drives green innovation, resulting in visible gains in ENP. In light of the discussion above, we put forth the following hypothesis:

H4. Green innovation positively mediates the relationship between EMA and ENP.

Corporate environmental ethics serve as a key driver for green innovation, improving sustainable performance while reflecting management’s commitment to environmental performance (Song and Yu, 2018). The formalization of environmental values and norms through corporate environmental ethics allows organizations to incorporate ecological principles across their operations, enabling long-term improvements in economic, social, and environmental performance (Alsayegh et al, 2020). Second, corporate environmental ethics play an important role in driving GI by methodically combining and maximizing various resources. Businesses that demonstrate genuine care for the environment are more inclined to devote effort to building eco-friendly operations (Baker et al, 2014). This dedication offers a solid foundation for assured green innovation, resulting in sustainable performance (Awan et al, 2021). Finally, leaders who prioritize environmental ethics use green innovation to develop policies that balance environmental, economic, and social performance while aligning with stakeholder expectations. Existing Literature shows that managers who value environmental ethics have a positive attitude toward society and the environment (Chang, 2011). Thus, by promoting an innovation culture, environmentally aware practices can replace inefficient techniques with innovative or improved systems, products, processes, and technologies, resulting in long-term benefits. Based on these ideas, this analysis forecasts the following relationships:

H5. GI mediates the relationship between environmental ethics and ENP.

According to Grant (1996), the Knowledge-Based View (KBV) emphasizes that human knowledge is a central strategic resource that enhances a firm’s competitiveness. Enterprises which must adhere to strict environmental standards place a high value on green human capital (GHC). Furthermore, firms that use GHC to tap into their workers’ talents, expertise, and inventiveness for environmental preservation are more likely to implement a GI strategy. They understand the substantial impact this technique may have on their environmental performance (Azunre et al, 2022). As a result, GHC helps firms to identify intangible assets, such as their employees’ environmental expertise, and promotes the execution of GI in the face of constant environmental demands to increase and sustain performance (AL-Khatib and Shuhaiber, 2022). Green relational capital (GRC) helps to promote green innovation by lowering transaction costs associated with searches, information, agreements, and transactions. Enterprises that adopt a GRC approach in their sustainable operations can attract environmentally conscious consumers and foster better green innovation, thereby reducing environmental impacts (Li et al, 2023). In the context of green structural capital (GSC), this refers to the codified environmental knowledge within the firm. Such knowledge is essential for driving GI, particularly in the development of new products (Fleming and Sorenson, 2004). GSC enhances the acquisition, assimilation, and application of green knowledge, thereby promoting innovation, improving coordination across research and development, and ultimately strengthening green performance (Wang and Juo, 2021). Therefore, based on the foregoing debate, we suggest this hypothesis:

H6. GI positively mediates the relationship between GIC and ENP.

Hierarchical and organizational support play a critical role in the effective implementation of development initiatives, including green innovation (Yang et al, 2017). Managerial backing is essential for fostering innovation and ensuring the success of green practices within the firm. Further advocating this stance, Adams et al (2016) posit that heightened managerial endorsement of green innovation facilitates more sustainable business practices. Firms have progressively acknowledged environmental concerns and sought to cultivate a dedicated approach to green management (Fineman and Clarke, 1996). Previous research confirms that managerial support for green innovation significantly influences the success of sustainable practices (Shahzad et al, 2020). MEC has been recognized as a key factor in eco-innovation, nurturing environmentally responsible behaviors and enhancing ENP (Guillard et al, 2018; Singh and Sahu, 2020). MEC reflects a firm’s capacity to integrate environmental considerations into strategic planning, thereby minimizing negative environmental impacts. Weng et al (2015) further highlight that the effectiveness of green innovation on environmental performance is strengthened when there is a high level of managerial commitment. Similarly, Rehman et al (2021) found that stronger environmental concern leads to enhanced performance in green innovation. Le et al (2022) reinforce this view, suggesting that firms with strong environmental ethics and a proactive green strategy achieve a competitive advantage through improved green innovation outcomes.

Based on this synthesis, we propose the following hypothesis:

H7: Managerial environmental concern positively moderates the relationship between GI and ENP.

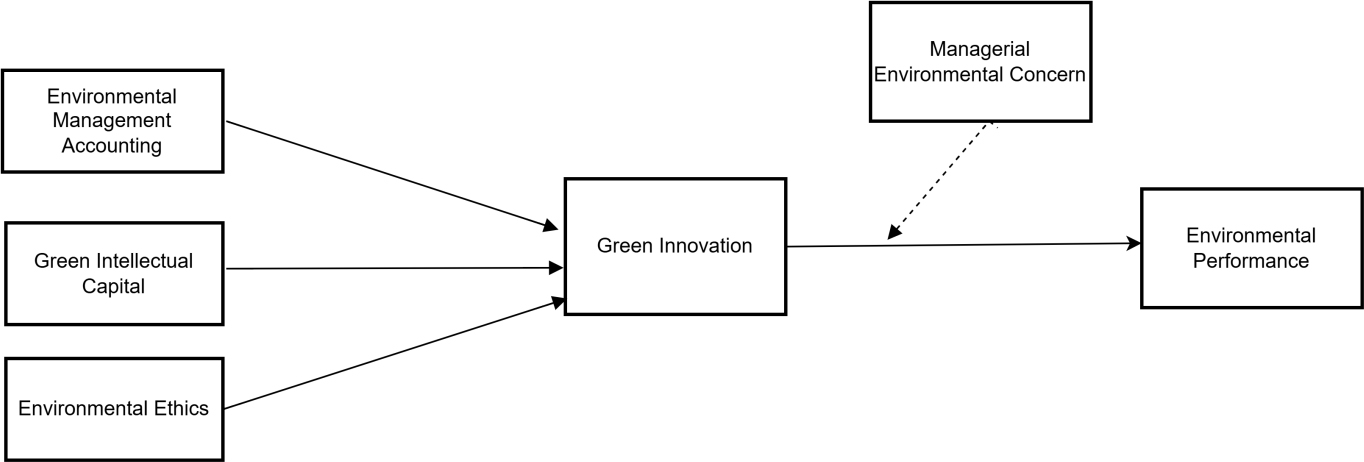

The present study investigates the influence of EMA, GIC, and ENETH on ENP, with GI as a mediator and MEC as a moderator, as shown in Fig. 1. A survey-based approach was adopted to collect primary data, which is appropriate for studies aiming to measure organizational-level perceptions across a large number of respondents. The sampling frame consisted of 582 ISO 14000-certified manufacturing firms in Pakistan, as these firms are more likely to engage in formalized environmental practices and are therefore relevant to the research objectives. A total of 560 questionnaires were distributed directly to finance managers and management accountants between September 2023 and January 2024. After screening for incomplete responses, 397 valid responses were retained for analysis.

Fig. 1.

Fig. 1.

Conceptual model.

We employed PLS-SEM using SmartPLS 4.0 (Version 4.0, SmartPLS GmbH, Hamburg, Germany) due to the complex nature of the model, which includes mediation and moderation relationships among multiple latent variables. PLS-SEM is preferred when the primary objective is prediction and theory development, particularly when the data do not meet multivariate normality and the sample size is moderate. This method also allows for robust analysis of hierarchical constructs and interaction effects, which are central to this study.

The final sample size of 397 valid responses meets the statistical requirements for PLS-SEM analysis. As the instrument included 36 items, and the maximum number of items for a single construct was 6, the sample exceeds the “10-times rule” (Hair et al, 2019). Additionally, sample size recommendations for detecting medium effect sizes with adequate statistical power (Cohen, 1992) suggest that a minimum of 320 responses is sufficient. Hence, our sample of 397 ensures the robustness of the model estimation and the generalizability of the results.

This study employed well-established constructs that were utilized in previous research to measure all the items (Appendix Table 7). The response for each item is measured on a “5 point Likert Scale”, with responses ranging from Strongly Disagree (1) to Strongly Agree (5). This study measured GIC as a second-order reflective construct because its three dimensions (GHC, GSC, and GRC) reflect the same meaning. This study borrowed a GIC scale consisting of 13 items to measure all three constructs of green intellectual capital. These consisted of five items to measure green human capital, five items to measure green structural capital, and three items to measure green relational capital, all initially developed by Hair et al (2019) and validated in many recent pieces of research (e.g., Asiaei et al, 2022b; Begum et al, 2023; Yong et al, 2020). A sample item of GIC includes “The productivity and contribution of employees concerning environmental protection in the company is better than those of its major competitors”. This study measured the EMA using a 6-item scale from Wang et al (2019). A sample item of EMA included “Our firm’s accounting system records all physical inputs and outputs (such as energy, water, materials, wastes, and emissions)”. This measure has been validated in many recent studies (e.g., Chaudhry and Amir, 2020; Zahoor and Gerged, 2021). ENETH is measured using a 4-item scale that has been utilized in various studies (Baah et al, 2024; Chang, 2011). A sample item of ENETH included “The company has clear and concrete environmental policies”. GI is measured using a 5-item scale adopted from extant literature (Chang, 2011), and used in recent studies by Bonsu et al (2024); Khan et al (2019); and Kraus et al (2020). A sample item of GI included “The company develops environmentally friendly products and services”. Four items of MEC are adopted from Eiadat et al (2008) and were recently used by Ar (2012) and Hojnik and Ruzzier (2016). A sample item of MEC included “Our top management demonstrates a strong commitment to environmental sustainability”. ENP is measured by a 4-item scale initially developed by Judge and Douglas (1998) and validated by recent research (Asiaei et al, 2022b, Asiaei et al, 2022c, Asiaei et al, 2023). A sample item of ENP included “Our organization complies with environmental regulations (i.e., emissions, waste disposal)”.

The Common Method Bias (CMB) problem in the dataset cannot be ignored; therefore, we estimated Harman’s Single Factor using SPSS (Version 26, IBM, Armonk, NY, USA). Factor Analysis was performed using all 36 items to extract one principal factor that explains the majority of the variance. The results indicated that the first factor is responsible for 43.55%, which is below the cut-off value of 50%. Consequently, it has been determined that there is no chance of a substantial impact of CMB on the estimated outcomes.

SmartPLS 4.0 was used to test the hypotheses. Data were analyzed using the PLS-SEM technique. This approach is used to test and analyze the problem under consideration. A two-step modeling approach is suggested by Hair et al (2019) to test the outer (measurement model) and inner (structural model). This study also employed a two-step approach. First, it tested the overall reliability, construct validity, and discriminant validity using the outer model (Begum et al, 2023). Then, we reported the results of a structural model.

Table 1 depicts the demographics of respondents for this study, showing that 56.2% of respondents are male and 43.8% are female. This reveals that, in manufacturing firms in Pakistan, the majority of finance managers and management accountants are male. As far as the age of the respondents is concerned, 29% of respondents fall into the first category, i.e., “Less than 40 years”, while the majority of the respondents (45.8%) belong to the second age category of “40–50 years”. Only 21.4% of respondents are in the age bracket of “50–60 years”. The minimum number of respondents (3.8%) is from the highest age category of “Above 60 years”. 17.6% of respondents are from the experience category of “Less than 10 years”. Additionally, 42.8% (the majority) of the respondents are from the second category of experience, i.e., “10–20 years”, 30% of respondents are from the experience bracket “20–30 years”, while the fewest (9.6%) have more than 30 years of experience.

| Respondent’s profile | Category | Frequency | Percentage |

| Gender | Male | 223 | 56.2 |

| Female | 174 | 43.8 | |

| Age | Less than 40 years | 115 | 29.0 |

| 40–50 years | 182 | 45.8 | |

| 50–60 years | 85 | 21.4 | |

| Above 60 years | 15 | 3.8 | |

| Experience | Less than 10 years | 70 | 17.6 |

| 10–20 years | 170 | 42.8 | |

| 20–30 years | 119 | 30.0 | |

| More than 30 years | 38 | 9.6 |

Table 2 depicts the individual loading of each item that is above the threshold value of 0.708 (Hair et al, 2019). Therefore, all the items were retained, and the reliability of each construct is measured by Cronbach’s alpha, which demonstrates that the value of each construct is greater than the threshold point of 0.70. As far as validity is concerned, the composite reliability (CR) of each construct also meets the said criterion, being greater than 0.7 and less than 0.95. Moreover, the convergent validity is assessed through the Average Variance Extracted (AVE), and the results indicate that the AVE for each construct is greater than 0.5. Therefore, these findings confirm the reliability and validity of all the constructs in this study. To check the discriminant validity, we applied the Heterotrait-Monotrait (HTMT) method in this study. The results in Table 3 show that the value is less than 0.85. Finally, the standardized root mean square residual (SRMR) is applied to assess the goodness of fit. The SRMR value for the current study is 0.061, which is less than the standard value of 0.08, indicating that the model is a good fit.

| Constructs | Items | Loadings | Cronbach’s alpha | CR | AVE |

| Environmental Management Accounting | EMA1 | 0.897 | 0.912 | 0.918 | 0.827 |

| EMA2 | 0.892 | ||||

| EMA3 | 0.887 | ||||

| EMA4 | 0.895 | ||||

| EMA5 | 0.937 | ||||

| EMA6 | 0.949 | ||||

| Green Human Capital | GHC1 | 0.806 | 0.918 | 0.921 | 0.758 |

| GHC2 | 0.930 | ||||

| GHC3 | 0.924 | ||||

| GHC4 | 0.927 | ||||

| GHC5 | 0.749 | ||||

| Green Relational Capital | GRC1 | 0.966 | 0.937 | 0.937 | 0.889 |

| GRC2 | 0.966 | ||||

| GRC3 | 0.895 | ||||

| Green Structural Capital | GSC1 | 0.976 | 0.927 | 0.927 | 0.913 |

| GSC2 | 0.986 | ||||

| GSC3 | 0.983 | ||||

| GSC4 | 0.981 | ||||

| GSC5 | 0.843 | ||||

| Environmental Ethics | ENETH1 | 0.964 | 0.932 | 0.932 | 0.923 |

| ENETH2 | 0.962 | ||||

| ENETH3 | 0.957 | ||||

| ENETH4 | 0.960 | ||||

| Green Innovation | GI1 | 0.921 | 0.947 | 0.947 | 0.825 |

| GI2 | 0.915 | ||||

| GI3 | 0.901 | ||||

| GI4 | 0.908 | ||||

| GI5 | 0.897 | ||||

| Managerial Environmental Concern | MEC1 | 0.903 | 0.905 | 0.925 | 0.727 |

| MEC2 | 0.920 | ||||

| MEC3 | 0.831 | ||||

| MEC4 | 0.879 | ||||

| Environmental Performance | ENP1 | 0.891 | 0.932 | 0.934 | 0.830 |

| ENP2 | 0.893 | ||||

| ENP3 | 0.927 | ||||

| ENP4 | 0.933 |

EMA, environmental management accounting; GHC, green human capital; GRC, green relational capital; GSC, green structural capital; ENETH, environmental ethics; GI, green innovation; MEC, managerial environmental concern; ENP, environmental performance. CR, Composite Reliability; AVE, Average Variance Extracted.

| Construct | EMA | ENETH | ENP | GHC | GI | GRC | GSC | MEC |

| EMA | - | |||||||

| ENETH | 0.392 | - | ||||||

| ENP | 0.559 | 0.805 | - | |||||

| GHC | 0.521 | 0.388 | 0.503 | - | ||||

| GI | 0.496 | 0.596 | 0.705 | 0.456 | - | |||

| GRC | 0.495 | 0.414 | 0.500 | 0.834 | 0.420 | - | ||

| GSC | 0.470 | 0.363 | 0.489 | 0.851 | 0.432 | 0.813 | - | |

| MEC | 0.085 | 0.268 | 0.351 | 0.133 | 0.171 | 0.122 | 0.090 | - |

HTMT, Heterotrait-Monotrait ratio of correlations.

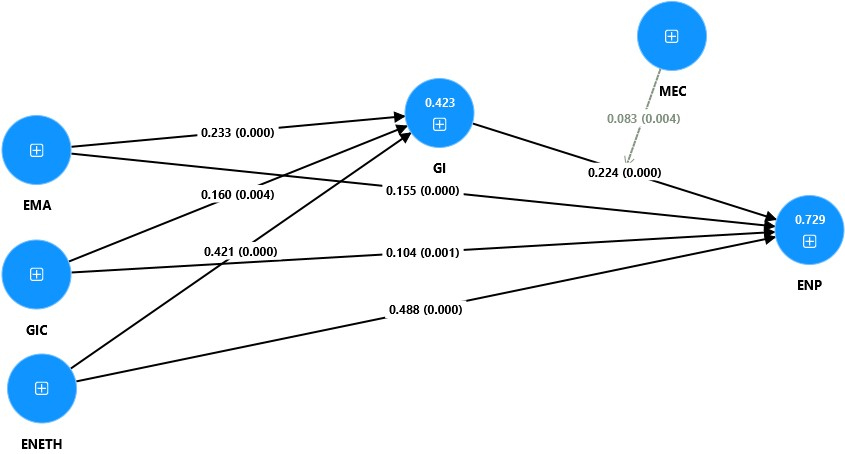

To test the hypothesis of this study, we used the bootstrapping technique. The

results of the structural model are shown in Fig. 2, which indicates that the

first hypothesis tests the direct impact of EMA on ENP. This impact is

significant (0.155, p

Fig. 2.

Fig. 2.

Results of structural model.

| Hypothesis | Hypothetical path | Beta | T-values | p values | Confidence interval | Results |

| H1 | EMA → ENP | 0.155 | 4.484 | 0.000 | 0.086–0.222 | Accepted |

| H2 | ENETH → ENP | 0.488 | 10.729 | 0.000 | 0.399–0.578 | Accepted |

| H3 | GIC → ENP | 0.104 | 3.348 | 0.001 | 0.045–0.164 | Accepted |

| H4 | EMA → GI → ENP | 0.052 | 3.249 | 0.001 | 0.025–0.087 | Partial Mediation |

| H5 | ENETH → GI → ENP | 0.194 | 4.191 | 0.000 | 0.154–0.243 | Partial Mediation |

| H6 | GIC→ GI → ENP | 0.036 | 2.636 | 0.008 | 0.011–0.064 | Partial Mediation |

| H7 | MEC |

0.083 | 2.877 | 0.004 | 0.029–0.140 | Moderated |

Variance Accounted for (VAF) Statistics is used to check the mediation results, which are calculated by dividing the indirect effect of each path by the total effect. The results are reported in Table 5, which clearly shows the presence of partial mediation in three mediation paths. The standard value to confirm the presence of full mediation is above 0.80. If the value is between 0.20 and 0.80, it indicates the presence of partial mediation. If the value is less than 0.20, according to the criteria, there will be no mediation. Therefore, H4, H5, and H6 are confirmed by the data.

| Independent variables | Dependent variable | Mediating variable | Indirect effect | Total effect | VAF (%) |

| EMA | ENP | GI | 0.052 | 0.207 | 0.2512 |

| GIC | ENP | GI | 0.194 | 0.682 | 0.2844 |

| ENETH | ENP | GI | 0.036 | 0.140 | 0.2571 |

VAF, Variance Accounted for.

Drawing on the Natural Resource-Based View (Hart, 1995), this study offers a unique perspective on how firms develop and leverage valuable environmental resources and capabilities to enhance their environmental performance. Our findings underscore the critical role of internal green practices—such as EMA, GIC, and ENETH—in driving GI, which in turn leads to ENP. The results further highlight the importance of MEC as a key moderator that strengthens the positive impact of GI. This aligns with NRBV’s emphasis on not only possessing valuable resources but also effectively deploying them through supportive leadership and organizational commitment.

Regarding H1, the findings indicate a positive and significant impact of EMA on ENP. This hypothesis is accepted, demonstrating that EMA helps monitor environmental impacts and allocate resources more efficiently, thereby fostering improvements in ENP. The findings of this study align closely with prior empirical studies (Appannan et al, 2023; Asiaei et al, 2022b). Our analysis indicates that organizations should consider adopting EMA to enhance the ENP. The findings of this study are consistent with prior empirical research that validates the significant role of EMA in enhancing ENP across various organizational and national contexts. The EMA serves not only as a compliance mechanism but also as a strategic tool that aligns environmental accountability with operational efficiency. This empirical evidence substantiates the argument that EMA contributes to improved ENP by providing better visibility into environmental costs and resource flows, leading to more informed and sustainable decision-making. Thus, our study contributes to the growing body of literature that positions EMA as a vital capability within the NRBV framework, reinforcing its importance in driving environmental sustainability in the manufacturing sector, especially within the emerging economic context of Pakistan.

The results for H2 confirm that ENETH positively influences ENP, supporting the NRBV perspective that ethical values are strategic internal resources that drive sustainability. Consistent with prior study (Singh et al, 2019), ENETH is an intangible asset that demonstrates a greater commitment to pollution control, resource protection, and sustainable practices. Our findings confirm that value-driven approaches significantly enhance ENP, highlighting the strategic importance of ethical resources in fostering long-term environmental and competitive outcomes, particularly in the context of emerging economies like Pakistan.

The results for H3 confirm that GIC positively and significantly influences ENP, aligning with the NRBV’s assertion that firms gain a sustainable competitive advantage through the development of unique environmental resources and capabilities (Hart, 1995; Russo and Fouts, 1997). Consistent with Asiaei et al (2022c), our results suggest that organizations that effectively acquire and deploy green knowledge and competencies are better positioned to reduce environmental costs and enhance eco-friendly practices. GHC, reflected in employees’ environmental expertise and commitment (Chang, 2016), drives the implementation of sustainable initiatives. GSC, which includes environmental management systems and supportive infrastructures (Chang and Chen, 2012), enables the systematic execution of green strategies. Meanwhile, GRC’s collaborative ties with stakeholders who share environmental goals foster environmental innovation and compliance (Hadj et al, 2020; Haldorai et al, 2022). Collectively, these components of GIC enhance a firm’s environmental reputation and operational efficiency, confirming GIC as a strategic resource for achieving superior ENP.

The findings for H4 confirm that GI positively mediates the relationship between EMA and ENP, aligning with the NRBV’s assertion that internal capabilities translate into sustainable outcomes through strategic deployment. EMA aids firms by providing detailed insights into environmental costs and resource flows, enabling the identification of inefficiencies and environmental impacts (Gomez-Conde et al, 2019). These insights serve as a foundation for GI by directing attention toward areas where technological, process, or product redesign can reduce environmental harm and improve efficiency (Benzidia et al, 2024). The results of this study support the view that EMA-driven data enables innovation by aligning environmental priorities with operational strategies (Guenther et al, 2016), fostering the development of eco-friendly alternatives that enhance ENP. Furthermore, as noted by Buhl et al (2016), such innovations not only yield environmental benefits but also strengthen a firm’s competitive positioning through increased brand credibility and stakeholder trust. Thus, GI acts as a mediator through which EMA contributes to superior environmental performance, reinforcing its strategic significance in sustainability-oriented firms.

The results of H5 confirm that GI positively mediates the relationship between ENETH and ENP, extending prior research by establishing GI as a key mechanism through which ethical orientations are translated into environmental performance. Consistent with NRBV logic, ENETH, formalized as shared environmental norms and values, serves as a strategic internal resource that drives innovation aimed at sustainability (Alsayegh et al, 2020; Song and Yu, 2018). Firms that internalize ethical commitments to ecological responsibility are more likely to invest in innovative processes, technologies, and product designs that align with stakeholder expectations and regulatory standards (Baker et al, 2014). Our findings, drawn from 397 Pakistani manufacturing firms, support the notion that such value-driven initiatives cultivate a culture of innovation that enhances resource efficiency, reduces ecological impact, and strengthens competitive positioning. By embedding environmental values into operational strategies, firms leverage green innovation as a means of achieving long-term environmental gains, thereby confirming the mediating role of GI in the ethics–ENP nexus (Awan et al, 2021). This contributes to the limited body of work linking internal ethical structures with clean manufacturing outcomes, highlighting the importance of managerial ethical leadership in fostering green innovation for sustainable performance.

The findings for H6 confirm that GI positively mediates the relationship between GIC and ENP, aligning with the KBV, which emphasizes knowledge as a critical strategic resource (Grant, 1996). As supported by Azunre et al (2022) and AL-Khatib and Shuhaiber (2022), firms leveraging GHC—employees’ environmental expertise and creativity—can more effectively translate environmental knowledge into innovative practices. Similarly, GSC, which encompasses codified environmental knowledge and systems, facilitates innovation by enhancing knowledge assimilation and coordination across green initiatives (Fleming and Sorenson, 2004; Wang and Juo, 2021). GRC strengthens external stakeholder linkages, reduces information costs, and enables more collaborative green solutions (Li et al, 2023). Together, these GIC components support the internal development of eco-innovative capabilities, which in turn drive improved environmental outcomes.

Supporting H7, the study also reveals that MEC positively moderates the relationship between GI and ENP, reinforcing prior findings that managerial commitment plays a pivotal role in the success of green innovation initiatives (Shahzad et al, 2020; Weng et al, 2015). When managers exhibit strong environmental values and integrate sustainability into strategic planning, the effectiveness of GI on ENP is significantly amplified (Rehman et al, 2021; Singh and Sahu, 2020).

This study investigates the impact of green practices (i.e., GIC, and ENETH) on ENP as well as the mediating role of green innovation and the moderating role of MEC in the manufacturing sector of Pakistan. The data were collected from 397 respondents, and SmartPLS 4.0 was used for analysis. Results indicate a positive and significant direct and indirect relationship between green practices (i.e., EMA, GIC, and ENETH) and ENP in the presence of GI as a mediating variable. The moderating effect of MEC is also significant in the relationship between GI and ENP. This study emphasizes the effective utilization of green practices and underscores the importance of green and intangible assets. The study recommends investing in GIC to foster GI, enhance environmental capabilities, and drive sustainability across operations. Similarly, organizations with strong ENETH are more inclined to integrate sustainability into their core values, policies, and operational frameworks. Moreover, integrating EMA into advanced accounting systems can help achieve environmental goals. This study aligns with the SDGs by promoting sustainable practices in Pakistan’s manufacturing sector.

This study supports SDG 8 (Decent Work and Economic Growth) by indicating that the integration of green practices (i.e., EMA, GIC, and ENETH) can create new green job opportunities, enhance productivity, and drive sustainability. It also supports SDG 9 (Industry, Innovation, and Infrastructure) by demonstrating that firms with GRC and innovation are more capable of investing in eco-friendly technologies and sustainable infrastructure. This study also supports SDG 12 (Responsible Consumption and Production), as EMA aids firms in diminishing waste, tracking environmental costs, and improving resource efficiency, thereby laying the foundation for circular economy practices and sustainable supply chains. This research highlights the need for both organizations and policymakers, particularly in developing economies like Pakistan, to highlight the strategic value of GIC, EMA, and GI in achieving environmental sustainability. Ultimately, this study provides practical insights for decision-makers aiming to align corporate operations with global sustainability objectives and promote long-term ecological and economic resilience.

This study provides a valuable theoretical contribution to the NRBV theory by deepening the understanding of how green practices (i.e., GIC, EMA, and ENETH) facilitate collaborative environmental problem-solving through waste reduction and emission control in the pursuit of ENP. From a managerial perspective, the findings highlight the need for proactive environmental considerations from top management and investment in green practices. Managers are encouraged to enhance their firms’ green practices by developing green technologies, sustainable products, and resource-efficient production systems—ultimately securing an ENP in a developing economy like Pakistan. Moreover, this study provides practical guidance for managers seeking to enhance ENP and sustainability within their organizations. Managers can integrate these green resources, such as GIC and EMA, to enhance the decision-making process and monitor environmental costs for improved sustainability. For example, manufacturing firms may initiate a sustainability-focused training program to promote energy-efficient production and effective waste management. Moreover, firms can track cost-saving opportunities by integrating EMA systems to provide clear insights into energy usage and material waste. For example, replacing outdated machinery with energy-efficient alternatives can simultaneously lower operational costs and carbon emissions. Ultimately, the synergy between green practices (i.e., EMA, GIC, and ENETH) facilitates the alignment of environmental objectives with core business strategies, fostering both sustainability and ENP.

This study, while insightful, has several limitations that offer avenues for future research. First, the analysis is limited to Pakistan’s manufacturing sector, which may constrain generalizability; future studies should replicate the model across different countries and industries. Second, although the sample size is statistically adequate, larger and more diverse samples would enhance external validity. Third, the cross-sectional design restricts causal inference. Longitudinal studies are recommended to capture the dynamic impact of green innovation on environmental performance over time. Finally, future research could expand the framework by exploring additional moderating variables, such as regulatory pressure and technological capability, as well as by examining broader performance outcomes. Despite these limitations, the study offers a novel moderated mediation model that can guide both scholars and practitioners in advancing sustainable business strategies.

Data is available on request to the corresponding author.

QT and KA were responsible for the conceptualization and design of the study, as well as the execution of data analysis. MHR and MSM contributed to data collection and provided overall project supervision. WR contributed to the writing and revision support of the manuscript. QT also led the funding acquisition efforts. All authors contributed to the critical revision of the manuscript, reviewed the final version, and approved it for submission. All authors have agreed to be accountable for all aspects of the work.

Not applicable.

This study was funded by the National Social Science Fund of China (No. 19AGL003) and the National Social Science Fund of China (No. 20&ZD127).

The authors declare no conflict of interest.

The authors declare that no generative artificial intelligence (AI) tools were used in the conceptualization, analysis, interpretation, or writing of this manuscript. The entire intellectual and scholarly content was developed solely by the authors. Where AI-assisted technologies (such as language editing tools or statistical software) were employed, their use was strictly limited to technical support and did not contribute to the creative or substantive elements of the research. The authors take full responsibility for the integrity and originality of the work presented.

| Variables | Definition | |

| Independent Variables | ||

| Environmental Management Accounting | Environmental Management Accounting refers to the process of identifying, collecting, analyzing, and reporting both environmental and financial information to support internal management decisions aimed at improving environmental performance and sustainability. EMA integrates traditional accounting with environmental data to help organizations monitor resource consumption, waste generation, and environmental costs, thereby facilitating more effective environmental management and strategic planning. | |

| Green Intellectual Capital | Green Intellectual Capital refers to the intangible assets and knowledge resources within an organization that are specifically related to environmental management and sustainability. It encompasses employees’ environmental skills and expertise (human capital), organizational routines and processes for green innovation (structural capital), and relationships with external stakeholders focused on environmental performance (relational capital). GIC enables firms to develop and implement eco-friendly strategies, improve resource efficiency, and gain competitive advantages through sustainable innovation. | |

| Environmental Ethics | Environmental Ethics is a branch of philosophy that examines the moral relationship between humans and the natural environment. It concerns principles and values guiding human behavior toward the environment, emphasizing responsibilities to protect, preserve, and sustainably manage natural resources. In organizational contexts, environmental ethics shapes corporate policies and practices by promoting ethical decision-making that balances economic goals with environmental stewardship and social well-being. | |

| Mediating Variable | ||

| Green Innovation | Green Innovation refers to the development and implementation of new or improved products, processes, practices, or technologies that reduce environmental impacts, enhance resource efficiency, and promote sustainable development. It encompasses eco-friendly solutions aimed at minimizing pollution, waste, and energy consumption, while fostering environmental sustainability and competitive advantage for organizations. | |

| Dependent Variable | ||

| Environmental Performance | Environmental Performance measures an organization’s effectiveness in managing and reducing its environmental impacts through its operations, products, and services. It typically includes indicators such as resource consumption (energy, water), waste generation, emissions, pollution control, and compliance with environmental regulations. Strong environmental performance reflects a firm’s commitment to sustainability and its ability to minimize negative effects on the natural environment. | |

| Moderating Variable | ||

| Managerial Environmental Concern | Managerial Environmental Concern refers to the degree to which an organization’s top managers recognize, prioritize, and actively support environmental issues within their strategic decision-making processes. It reflects managers’ awareness and commitment to integrating environmental sustainability into business objectives, policies, and practices, which can influence the firm’s environmental performance and adoption of green innovations. | |

| Construct | Adapted Source | |

| Environmental ManagementAccounting | Wang et al (2019) | |

| EMA1 | Our firm’s accounting system recording all physical inputs and outputs (such as energy, water, materials, wastes, and emissions). | |

| EMA2 | Our firm’s accounting system can carry out product inventory analyses, product improvement analysis, and product environmental impact analysis. | |

| EMA3 | Our firm using environmental performance targets for physical inputs and outputs. | |

| EMA4 | Our firm’s accounting system can identify, estimate, and classify environmental‐related costs and liabilities. | |

| EMA5 | Our firm’s accounting system can create and use of environmental‐related cost accounts. | |

| EMA6 | Our firm’s accounting system can allocate environmental‐related costs to products. | |

| Green Human Capital | Asiaei et al (2022b); Begum et al (2023); Yong et al (2020) | |

| GHC1 | The productivity and contribution of employees concerning environmental protection in the company is better than those of its major competitors. | |

| GHC2 | The employees’ competence of environmental protection in the company is better than that of its major competitors. | |

| GHC3 | The products and services of environmental protection provided by the employees of the company are better than those of its major competitors. | |

| GHC4 | The cooperative degree of team work pertaining to environmental protection in the company is more than that of its major competitors. | |

| GHC5 | Managers in the company can fully support their employees to achieve the goals of environmental protection. | |

| Green Structural Capital | ||

| GSC1 | The management system of environmental protection in the company is better than that of its major competitors. | |

| GSC2 | The company’s profit earned from environmental protection activities is more than that of its major competitors. | |

| GSC3 | The company’s ratio of environmental protection investments in R&D to its sales is more than that of its major competitors. | |

| GSC4 | Innovations about environmental protection in the company are more than those of its major competitors. | |

| GSC5 | Investments in environmental protection facilities in the company are more than those of its major competitors. | |

| Green Relational Capital | ||

| GRC1 | The company designs its products or services in compliance with the environmental desires of its customers. | |

| GRC2 | The company’s cooperative relationships about environmental protection with its upstream suppliers and downstream clients are stable. | |

| GRC3 | The company has stable and cooperative relationships about environmental protection with its strategic partners. | |

| ENETH | Baah et al (2024) | |

| ENETH1 | The company has clear and concrete environmental policies. | |

| ENETH2 | The company’s budget planning includes the concerns of environmental investment or procurement. | |

| ENETH3 | The company has integrated its environmental plan, vision, or mission to its marketing events. | |

| ENETH4 | The company has integrated its environmental plan, vision, or mission to company’s culture. | |

| GI | Bonsu et al (2024); Khan et al (2019); Kraus et al (2020) | |

| GI1 | The company develops environmentally friendly products and services. | |

| GI2 | The company implements processes that reduce environmental impact. | |

| GI3 | The company adopts technologies that contribute to sustainability. | |

| GI4 | The company integrates environmental considerations into its business strategies. | |

| GI5 | The company is committed to continuous improvement in environmental performance. | |

| MEC | Ar (2012); Hojnik and Ruzzier (2016) | |

| MEC1 | Our top management demonstrates a strong commitment to environmental sustainability. | |

| MEC2 | Environmental issues are a major consideration in our company’s strategic decisions. | |

| MEC3 | Management actively supports initiatives that reduce the company’s environmental impact. | |

| MEC4 | Managers encourage employees to engage in environmentally responsible behaviors. | |

| ENP | Asiaei et al (2023) | |

| ENP1 | Our organization complies with environmental regulations (i.e., emissions, waste disposal). | |

| ENP2 | Our organization limits environmental impact beyond compliance. | |

| ENP3 | Our organization prevents and mitigates environmental crises (i.e., significant spills). | |

| ENP4 | Our organization educates employees and the public about the environment. | |

References

Publisher’s Note: IMR Press stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.