, Juan Du 2,*

, Juan Du 2,* , Xiaoyan Liu 2

, Xiaoyan Liu 21 School of Innovation and Entrepreneurship, Hubei University of Technology, 430068 Wuhan, Hubei, China

2 School of Business Administration, Jianghan University, 430056 Wuhan, Hubei, China

Abstract

As a global manufacturing leader, China faces significant challenges in implementing green supply chain management (GSCM) to mitigate environmental impacts. This study proposes a holistic framework integrating management support, financial support, and supply chain e-linkage to examine their effects on green supply chain (GSC) practices among small and medium-sized enterprises (SMEs) in China’s key manufacturing regions. Using a mixed-methods approach, we analyzed 211 valid responses collected in two phases from 2022 to 2023, assessing the relationship between organizational support and GSC practices, as well as the contingent effects of e-linkage. The findings indicate that management support consistently strengthens supplier, internal, and customer green practices, while financial support significantly facilitates GSC implementation—underscoring that while managerial commitment is essential, it cannot substitute for targeted capital investment. Drawing on resource dependence theory, we caution firms to heed the dual nature of supply chain e-linkage: while it generates synergistic benefits through enhanced resource integration, it also poses risks by enabling adversarial tactics and power imbalances, especially in interactions with supply chain partners.

Keywords

- supply chain e-linkage

- organizational support

- green supply chain practices

- the contingent impact

Satellite data from the National Aeronautics and Space Administration (NASA) have revealed unprecedented reductions in air pollution across China, India, and the United States during the COVID-19 pandemic. This finding underscores the profound influence of supply chain activities on environmental outcomes, which are estimated to account for over 90% of a typical firm’s impact on air and water resources (Kitsis and Chen, 2021). The COVID-19 crisis, in particular, highlighted the urgent need to integrate sustainability into supply chain management, prompting firms to reassess their environmental footprint and adopt greener practices (Acquah et al, 2021; Yu et al, 2021). Despite reports of increasing firm proactivity (Jiang et al, 2020), the widespread adoption of green supply chain management (GSCM) practices remains limited. Choudhary and Sangwan (2022) further observe that green supply chain (GSC) practices are far from uniformly implemented across industries or regions. A key obstacle to broader uptake lies in the substantial resources required—encompassing financial investment, managerial commitment, and technological upgrades—which hinder many firms from fully realizing the significant benefits these practices offer.

This challenge is particularly acute in emerging markets. As documented in a comprehensive review by Geng et al (2017), these regions have become the world’s primary manufacturing centers, largely due to the relocation of production from developed nations seeking lower costs. Consequently, firms in these economies face escalating pressure to adopt green practices due to heightened global environmental awareness. However, this external pressure often conflicts with the national mandate to maintain rapid economic growth, forcing managers to balance environmental stewardship with economic performance. This conflict is further compounded by the distinct context of emerging markets, which, as Marquis and Raynard (2015) detail, are frequently characterized by weaker regulatory infrastructures, market volatility, and other significant institutional challenges. This dynamic creates an acute tension between global environmental imperatives and the operational and economic realities on the ground. This uneven progress raises a persistent question for both managers and researchers: how can firms effectively achieve environmental goals despite these challenges? Despite decades of exploration (Khan et al, 2021; Khurshid et al, 2024; Preuss, 2005), the specific mechanisms through which firms in these challenging contexts can leverage limited resources to overcome implementation barriers remain poorly understood (Graham, 2020).

In such resource-constrained settings, the strategic deployment of collaborative and digital tools is not merely an option, but a necessity. Information and communication technology (ICT), specifically supply chain e-linkage, has been proposed as a potential solution to overcome the inherent structural barriers of these markets. E-linkage provides a digital framework to enhance integration and, crucially, to optimize the deployment of scarce resources (Zhao et al, 2023). The experience of an emerging-market champion like Huawei offers a compelling illustration. By embedding ICT across its supply chain, the company built a transparent system—termed “black soil” in its 2018 Corporate Social Responsibility (CSR) Report—that optimizes resource use while fostering deeper collaboration with partners. Such collaboration is widely seen as vital for overcoming communication barriers and improving visibility within GSCM.

Yet, the benefits of e-linkage are not unequivocal, and these relational risks may be amplified in emerging market contexts. The same power imbalances and misaligned goals identified in the literature (Feng et al, 2020; Kumar et al, 2023) are likely to be exacerbated in these settings. Emerging market environments are often characterized by underdeveloped formal institutions, leading to weaker legal recourse and a greater reliance on informal, relational governance to navigate lower levels of generalized trust (Peng et al, 2008). This highlights the paradoxical nature of digital collaboration, particularly within the volatile settings of emerging economies, and underscores the need for a deeper understanding of how e-linkage interacts with other factors—such as a firm’s resource inputs—to influence GSC practices. To date, little research has explored how a digital ecosystem moderates this relationship between resource inputs (e.g., financial investments or managerial support) and GSC practices. While prior studies have illuminated managerial support’s influence on GSC adoption (Ilyas et al, 2020; Karim et al, 2024), they often overlook the financial investments required.

Although macro-level green finance policies encourage sustainable practices at regional or industrial levels (Wang et al, 2024), empirical evidence on the role of firm-level financial support in GSCM remains particularly scarce. This study contributes to ongoing discourse by developing a framework that integrates management support, financial backing, and IT adoption—specifically e-linkage—in shaping GSC practices. This study is therefore situated in emerging markets to provide an ideal empirical setting to investigate this theoretical paradox. It is precisely in these contexts—where resource constraints are acute, the need for efficiency is paramount, and the risks of dependency are high—that the competing pressures of collaboration and opportunism are most salient. In doing so, we address a direct call from Agyemang et al (2018) to investigate financial support’s role in these challenging environments. By examining the dichotomous (synergistic vs. antagonistic) moderating effects of e-linkage, this study offers both theoretical advancements and practical insights for effective resource allocation.

The paper proceeds as follows: Section 2 presents hypotheses along with their rationales; Section 3 outlines research methodology alongside initial observations; Section 4 details analyses and results; Section 5 offers conclusions alongside an in-depth discussion; finally, Section 6 outlines limitations while suggesting avenues for future research.

GSCM has emerged as an influential management paradigm within modern manufacturing. Central to GSCM are ‘GSC practices’, which, for the purpose of this study, are defined as the integration of environmental considerations into all phases of the supply chain (Srivastava, 2007). Aligning with established literature (Wong et al, 2015), we operationalize this construct across three distinct segments: upstream (supplier-focused), internal (firm-focused), and downstream (customer-focused). These segments collectively encompass a range of activities such as environmental collaboration, sustainable resource design, green procurement, and developing closed-loop systems for material recovery (Agyabeng-Mensah et al, 2021; Sarkis et al, 2011; Zhu et al, 2012), all of which aim to minimize ecological footprints.

The successful implementation of such multifaceted GSC practices is widely recognized as being contingent upon robust management support. This is because GSC initiatives represent significant organizational change that demands both strategic guidance and operational enablement. Firstly, implementing GSC practices—such as investing in cleaner technologies, training employees, or auditing suppliers—requires substantial financial, human, and technological resources. Only senior leadership possesses the authority to allocate these critical resources and signal to the entire organization that environmental performance is a strategic priority, not merely a peripheral concern (Mangla et al, 2014).

Furthermore, management support is essential for overcoming organizational inertia and fostering cross-functional integration. GSC practices inherently disrupt established routines and require deep collaboration across traditionally siloed departments like procurement, logistics, design, and marketing. Strong leadership is crucial to champion these changes, resolve inter-departmental conflicts, and build a cohesive, environmentally-conscious culture (Tseng et al, 2019). This is often operationalized through the establishment of comprehensive systems, such as Total Environmental Quality Management (TEQM), which institutionalize environmental responsibilities and facilitate continuous improvement (Green et al, 2019; de Sousa Jabbour et al, 2014). Finally, management is also responsible for navigating the external environment, ensuring that the firm’s green initiatives align with or exceed governmental standards and regulatory requirements (Saeed et al, 2018; Zhu et al, 2017b).

Collectively, the literature converges on the idea that management support acts as the foundational driver for GSC transformations. It provides the vision, resources, and structural mechanisms necessary to translate environmental intentions into tangible supply chain practices (Huang et al, 2017). Hence, we propose the following:

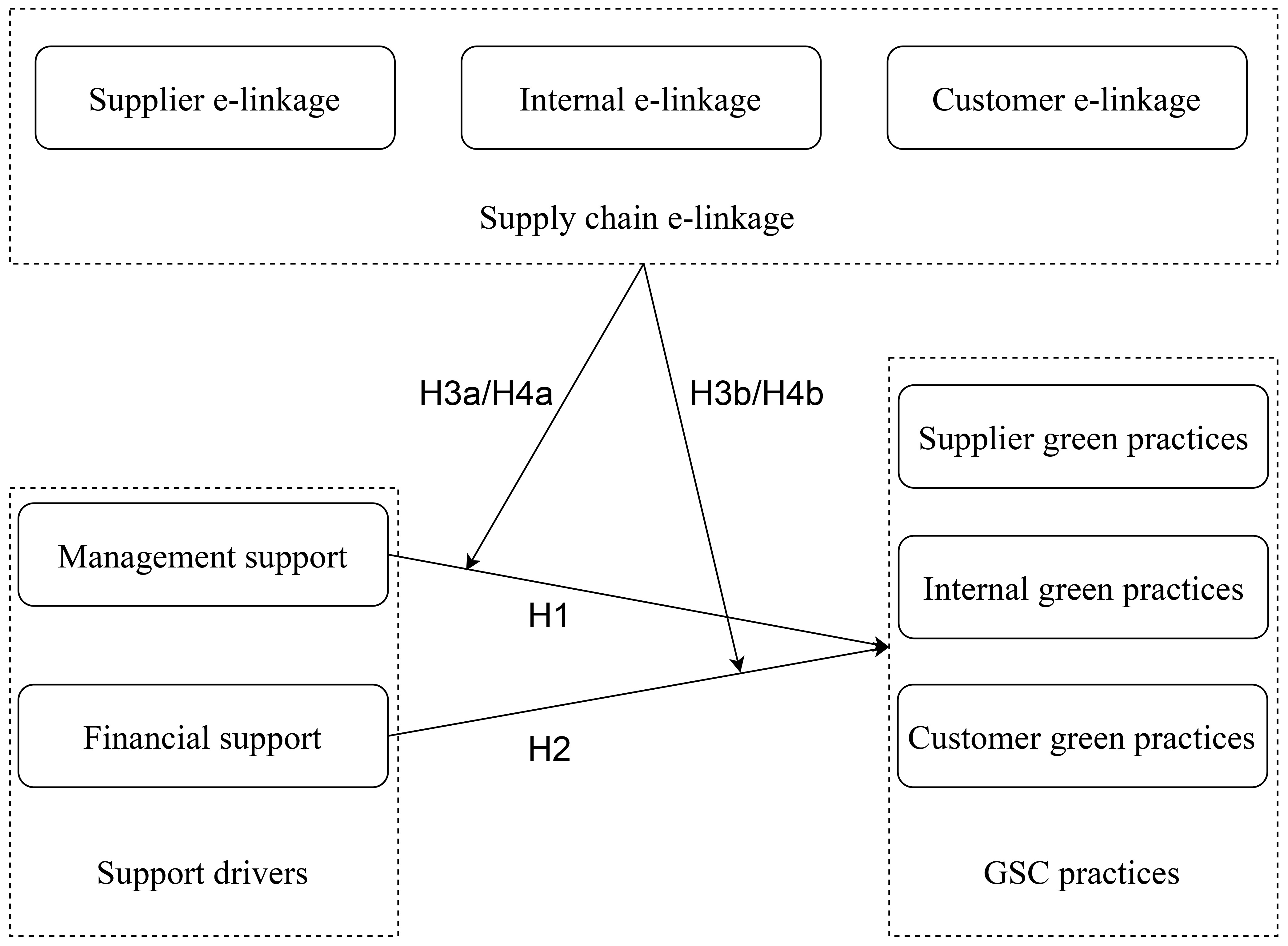

Hypothesis 1: Management support is directly and positively associated with GSC practices.

Beyond managerial commitment, the implementation of GSC practices is fundamentally constrained by economic and financial realities (Table 1). A substantial body of literature identifies financial constraints as one of the most significant barriers to GSC adoption (Govindan et al, 2014; Walker et al, 2008). These constraints manifest as high direct costs for environmentally friendly materials and packaging (Zhu and Sarkis, 2006), as well as the substantial initial capital investment required for green technologies and process redesign. Consequently, many firms face a strategic dilemma: despite the potential for long-term cost savings from waste reduction and closed-loop systems, the immediate pressures of investment uncertainty and funding challenges often lead them to deprioritize or delay their green initiatives.

| Research perspective | Drivers & Barriers for GSC practices | Associated references | |

| Direct influential factors | Internal level | Certification: ISO14001 | Arimura et al (2011) |

| Environmental concerns: Missions; Reputation; Responsibility; Resources scarcity | Zhu and Sarkis (2006); Abdullah et al (2018); Choudhary and Sangwan (2019); Dubey et al (2017); Huang et al (2017); Tachizawa et al (2015); Testa and Iraldo (2010); Zhu et al (2017a); Hsu et al (2013); Kohli and Hawkins (2015) | ||

| Managerial aspects: Top- and mid- commitment; TEQM; Departments collaboration; Internal impetus; social capital | Abdullah et al (2018); Agarwal et al (2018); Choudhary and Sangwan (2019); Chu et al (2017); Dubey et al (2017); Huang et al (2017); Mitra and Datta (2014); Luo et al (2015); Hung et al (2014); Tachizawa et al (2015); Zhu et al (2017a); Ye et al (2013); Green et al (2019); Kohli and Hawkins (2015) | ||

| Economic concerns: Cost savings; Profitability; Cost increasing | Choudhary and Sangwan (2019); Dubey et al (2017); Testa and Iraldo (2010); Wang et al (2018); Kohli and Hawkins (2015); Zhu and Sarkis (2006) | ||

| ICT: green information system & Tech | Green et al (2012); Savita et al (2016); Mendoza-Fong et al (2018) | ||

| Company characters | Choudhary and Sangwan (2019); Kuei et al (2015) | ||

| Others: JIT; GHRM | Song and Choi (2018); Zaid and Sleimi (2021); Green et al (2019); Kuei et al (2015); Liu et al (2012) | ||

| External level | Institutional aspects: Pressures; National (local) environmental regulations | Zhu and Sarkis (2006); Abdullah et al (2018); Agarwal et al (2018); Choudhary and Sangwan (2019); Dubey et al (2017); Huang et al (2017); Vanalle et al (2017); Xu et al (2013); Yang (2018); Zhu et al (2017a); Hoejmose et al (2014); Kohli and Hawkins (2015); Saeed et al (2018); Ahmed et al (2020) | |

| Market aspects: Market share; Product requirements | Zhu and Sarkis (2006); Agarwal et al (2018); Dubey et al (2017); Huang et al (2017); Tachizawa et al (2015); Testa and Iraldo (2010); Wang et al (2018); Hsu et al (2013); Kohli and Hawkins (2015); Kuei et al (2015); Liu et al (2012); Choi et al (2018) | ||

| Stakeholders: NGOs; Medias; Investors & subsides; Competitors; Supplier & customer pressures | Huang et al (2017); Tachizawa et al (2015); Testa and Iraldo (2010); Zhu et al (2017a); Hsu et al (2013); Liu et al (2012); Zhu and Sarkis (2006); Agarwal et al (2018); Kuei et al (2015) |

GSC, green supply chain; TEQM, total environmental quality management; ICT, information and communication technology; JIT, just in time; GHRM, green human resource management; NGOs, non-governmental organizations.

From a resource-based perspective, overcoming this hurdle requires more than just available cash; it demands a strategic allocation of financial support to build critical green capabilities. For instance, successfully adopting green procurement strategies necessitates dedicated investments in supplier environmental audits, specialized employee training, and the re-engineering of internal operational processes (Agyemang et al, 2018; Bai et al, 2023). Without such targeted financial resources, even the most well-intentioned GSC strategies are unlikely to be realized. This view is forcefully articulated by Sarpong and Oppong (2023), who assert that “the availability of financial resources is a crucial resource that motivates the adoption of green supply chain management strategies”, a claim consistently supported by recent study (Lai et al, 2023). Based on this compelling evidence, we propose the following:

Hypothesis 2: Financial support is directly and positively associated with GSC practices.

Numerous specific challenges arise in the implementation of GSC practices, including green material selection, green procurement, green production planning, green packaging, green transportation, and green distribution, among others. Management and financial support encompass the human, material, and financial resources that firms must initially invest to implement these GSC practices. According to de Camargo Fiorini and Jabbour (2017), there may be additional critical environmental variables or enablers beyond the aforementioned resource portfolio when implementing GSC practices, such as an electronic-integration environment. Through data exchange technology—based on a robust database and unified data transmission specifications in a highly collaborative environment—firms can leverage their critical support resources to fully utilize GSC practices. Supply chain e-linkage, referred to as a transactional linkage, involves planning and executing integrated business processes and operations that interact with internal and external partners, enabled by ICT. This has become a novel feature of the supply chain collaborative environment and has garnered attention from GSCM scholars (Małys, 2022). In practice, Mercedes-Benz collaborates closely with suppliers and customers, utilizing ICT to link processes and implement green principles. The increased transparency and visibility facilitated by a high level of e-linkage make management and financial support for green principles more effective and efficient (Daimler Annual Report, 2018, p. 106).

Consistent with the literature, managing and monitoring orders, packaging, distribution, transportation, storage, and return functions using ICT can be regarded as important features of supply chain e-linkage (Zhao and Liu, 2024). Furthermore, this paper aligns with the aforementioned study (Huo, 2012) in three key aspects: internal e-linkage, supplier e-linkage, and customer e-linkage.

Gold et al (2010) stated that “adequate resources facilitate environmentally sound corporate and supply chain behavior…the crucial intra-firm and inter-firm resources are prerequisites for implementing green practices, which may, in turn, represent sources of competitive advantage”. Both the Resource-Based View (RBV) and the Relational View (RV) focus on the effective and efficient use of valuable resources—internally and cooperatively—to enable a firm to outperform its rivals (Barney, 1991; Dyer and Singh, 1998).

In orchestrating the firm’s resources to implement green strategies, managers must select, develop, and bundle both internal and external resources. While the importance of management resources and financial investments controlled by the focal firm is undeniable, external resources shared with supply chain partners are often equally critical. According to prior study, supply chain e-linkage stands out as a significant resource, both internally and externally, emphasizing the capability to transform or optimize intra- and inter-organizational processes (Zhang et al, 2016). Consequently, supply chain e-linkage, when combined with the focal firm’s efforts, influences GSC practices through interaction. In other words, supply chain e-linkage among firms and internal departments enhances both visibility and communication. This, in turn, greatly improves the efficiency of management and financial support. As a result, a higher level of supply chain e-linkage leads to more effective management and financial support for GSC practices. This reasoning underpins the following hypothesis.

Hypothesis 3 (a, b): The positive relationship between support resources—including management (a) and finance (b)—and GSC practices is strengthened by higher levels of supply chain e-linkage, such that the impact of management and financial support on GSC practices increases as e-linkage increases.

Resource Dependence Theory (RDT) posits that firms within a supply chain can enhance their competitive advantage by fostering interdependence and effective collaboration (Sarkis et al, 2011). This mainstream perspective emphasizes that mutual reliance strengthens partnerships, enabling firms to leverage shared resources and capabilities. However, dependency asymmetry—where one party relies more heavily on another—can introduce power imbalances within these relationships (Hofer, 2015). According to RDT, power is defined as control over valued resources, granting the controlling party the ability to influence the behavior of others. This dynamic becomes particularly evident when a firm is deeply integrated with its supply chain partners or exhibits a high degree of e-linkage, making it challenging to switch partners due to entrenched dependencies.

In the context of green supply chain practices, such power imbalances can complicate sustainability efforts. Numerous challenges may arise during the implementation of green processes, prompting a firm with a dependency advantage to adopt strategies such as adversarial tactics or “free riding” to minimize profit losses. RDT suggests that unequal power dynamics dictate the allocation and effectiveness of critical resources, such as management support and financial support. When power is skewed, these resources may not be fully utilized to advance GSC initiatives, significantly undermining their impact (Touboulic et al, 2014). A substantial body of research has explored these power dynamics in supply chain relationships, frequently highlighting their detrimental effects (Caniëls and Gelderman, 2007).

A practical example can be observed in Apple Inc.’s global supply chain. Despite its advanced e-linkage capabilities, only 23 of its hundreds of partners are fully synchronized with its green management initiatives through management and financial investments (Apple Environmental Responsibility Report, 2018, p.4). This disparity suggests that high levels of e-linkage, while fostering integration, may not uniformly translate into effective support for sustainability goals across all partners. Based on this observation, the following hypothesis is proposed:

Hypothesis 4 (a, b): The positive relationship between support resources—including management (a) and finance (b)—and GSC practices is weakened by higher levels of supply chain e-linkage, such that the impact of management and financial support on GSC practices decreases as e-linkage increases.

The conceptual model, which integrates the relationships derived from the previous analysis, is presented in Fig. 1.

Fig. 1.

Fig. 1.

The conceptual model.

The survey instrument was developed following a rigorous three-step process adapted from Lietz (2010). First, an extensive literature review was conducted to identify and define the core constructs. As established measurement scales suitable for our specific research context were not fully available, items were carefully synthesized and adapted from prior influential studies. The conceptual definition and operationalization of each key variable are detailed below.

Management Support. We define management support as the set of strategic and operational commitments a firm makes to embed environmental thinking into its operations. This construct encompasses three core dimensions: (1) executive commitment, (2) systemic implementation, and (3) organizational integration. The measurement items were synthesized and adapted from several established studies, primarily drawing from Green et al (2019), Tseng et al (2019) and Zhu et al (2008).

Financial Support. Financial support is defined as the dedicated allocation of a firm’s capital resources toward GSCM implementation. Drawing on the RBV, we conceptualize this not as mere financial slack, but as a strategic investment aimed at building green capabilities (Barney, 1991). The items for this construct were adapted from scales in prior GSCM research, including the work of Zhu and Sarkis (2006), Walker et al (2008), Agyemang et al (2018) and Sarpong and Oppong (2023).

GSC Practices. GSC practices are defined as the integration of environmental considerations into all phases of the supply chain (Srivastava, 2007). In line with the literature (Wong et al, 2015), we operationalize GSC practices across three distinct segments: upstream (suppliers), internal (focal firm), and downstream (customers). The measurement items for these dimensions were synthesized from scales used by Zhu et al (2017b), Schmidt et al (2017), Acquah et al (2021) and Wang et al (2018).

Supply Chain E-linkage. We define supply chain e-linkage as the extent to which a firm utilizes ICT to integrate data and processes with its supply chain partners (Frohlich, 2002). This integration is operationalized by measuring the use of ICT for a range of key supply chain functions, such as the management of orders, distribution, and storage. This approach is consistent with a significant stream of research on IT-enabled supply chain integration that has examined these operational linkages (Frohlich, 2002; Ganbold et al, 2021; Huo, 2012; Liu et al, 2015). Following prior typologies in the supply chain integration literature (Ganbold et al, 2021), this study conceptualizes and examines e-linkage across three distinct dimensions: internal e-linkage, supplier e-linkage, and customer e-linkage.

Following the initial item generation, the second step involved a rigorous translation and pilot-testing process. The English questionnaire was translated into Chinese and then back-translated into English by independent academics to ensure conceptual equivalence. Third, the instrument was pilot-tested with twenty managers to refine the clarity and relevance of the items for the Chinese manufacturing context.

Finally, given that our scales were synthesized from multiple sources, we conducted an Exploratory Factor Analysis (EFA) on the pilot data as a preliminary check (The detailed EFA results can be found in Appendix Table 9). The EFA confirmed that the items for each construct loaded cleanly onto their intended factors, providing initial evidence of the scales’ factorial validity before proceeding with the main analysis.

Data for this study were collected from manufacturing firms in China, a critical context for GSCM given its global manufacturing role. The sample was drawn specifically from two of China’s most vital economic hubs: the Yangtze River Delta and the Pearl River Delta. These regions were chosen for their high concentration of manufacturing output, industrial diversity, and representativeness of the national landscape (iResearch, 2022).

The absence of a comprehensive database for manufacturing firms, particularly small and medium-sized enterprises (SMEs), precluded the use of random sampling. Consequently, region-specific strategies were adopted. In the Yangtze River Delta region, face-to-face surveys conducted at the 2022–2023 Yangtze River Delta Digital Transformation Conference yielded 124 valid questionnaires. In the Pearl River Delta, the absence of an analogous industry association necessitated the adoption of alternative strategies. Data collection primarily relied on industry conferences and corporate forums, with over 200 questionnaires systematically distributed through organizations such as the Guangdong Gaozhi Research Institute, Wuhan Fanuc Robot Co., Ltd., and a small and medium-sized enterprise (SME) in the technology sector based in Chengdu. Post-event follow-up via emails and telephone calls enhanced response rates, yielding 76 valid responses and a robust dataset for analysis. To counter survey biases, we followed Tehseen et al (2017) by employing diverse response formats and multiple data sources. A second phase in 2022–2023 analyzed annual reports from 30 listed SMEs, yielding 11 valid data points to strengthen the dependent variable’s validity.

A total of 211 valid responses were obtained across both data collection phases. Respondents comprised 84 middle managers (39.81%) and 127 senior managers (60.19%). By professional role, the sample included 9 production managers (4.27%), 31 sales managers (14.69%), 26 marketing and public relations managers (12.32%), 39 supply chain managers (18.48%), 84 administrative managers (including top-level and senior executives) (39.81%), 10 human resources managers (4.74%), and 12 research and development technicians (5.69%). In terms of gender, 168 respondents identified as male (79.62%). Firms primarily operated in auto parts, the light-emitting diode (LED)/semiconductors, and machinery/equipment/heavy industries, mirroring regional industrial patterns. Detailed profiles are in Table 2.

| Industry type | Num. Respondents | %Respondents | |

| IT/hardware/e-commerce | 13 | 6.16 | |

| Fast-Moving Consumer Goods | 9 | 4.27 | |

| Clothing/leather | 14 | 6.64 | |

| Furniture | 7 | 3.32 | |

| Home appliance | 5 | 2.37 | |

| Telecommunication | 12 | 5.69 | |

| Auto-parts | 19 | 9.00 | |

| LED/Semiconductor | 52 | 24.64 | |

| Machinery/Equipment/Heavy | 31 | 14.69 | |

| Bioengineering | 4 | 1.90 | |

| Medical equipment | 11 | 5.21 | |

| Transport and logistics | 4 | 1.90 | |

| Energy and chemical | 18 | 8.53 | |

| Others | 12 | 5.69 | |

| Listed or not | Num. Respondents | %Respondents | |

| Listed | 32 | 15.17 | |

| Not listed | 179 | 84.83 | |

| Location | Num. Respondents | %Respondents | |

| Chengdu | 18 | 8.53 | |

| Foshan | 22 | 10.43 | |

| Fuzhou | 23 | 10.90 | |

| Guangzhou | 33 | 15.64 | |

| Huizhou | 19 | 9.00 | |

| Shanghai | 17 | 8.06 | |

| Shenzhen | 34 | 16.11 | |

| Wuhan | 37 | 17.54 | |

| Yichang | 5 | 2.37 | |

| Others | 3 | 1.42 | |

| National high-tech firm certification | Num. Respondents | %Respondents | |

| Yes | 51 | 24.17 | |

| No | 160 | 75.83 | |

| Employees (3Y average) | Num. Respondents | %Respondents | |

| 28 | 13.27 | ||

| 50–99 | 52 | 24.64 | |

| 100–199 | 45 | 21.33 | |

| 200–499 | 47 | 22.27 | |

| 500–999 | 39 | 18.48 | |

| N/A | N/A | ||

| Total sales* (RMB: million) (3Y average) | Num. Respondents | %Respondents | |

| 2 | 0.95 | ||

| 5–10 | 6 | 2.84 | |

| 10–20 | 10 | 4.74 | |

| 20–50 | 53 | 25.12 | |

| 50–100 | 68 | 32.23 | |

| 100–400 | 60 | 28.44 | |

| 400 or more | 2 | 0.95 | |

| Missing data | 10 | 4.74 | |

| Ownership | Num. Respondents | %Respondents | |

| State-owned firm | 11 | 5.21 | |

| Private firm (China mainland) | 149 | 70.62 | |

| Joint venture firm | 9 | 4.27 | |

| Overseas-funded firm | 42 | 19.91 | |

| Supplier | 58 | 27.49 | |

| Midstream | 129 | 61.14 | |

| Customer | 24 | 11.37 | |

*In accordance with the “Statistical Classification of Large, Medium, Small, and Micro Enterprises (2017)” published by the National Bureau of Statistics of China, enterprises operating within the industrial sector with annual sales totaling 400 million yuan (approximately 5.8 million dollars) fall within the category of small and medium-sized enterprises (SMEs).

The average USD/CNY exchange rate for 2023 was 7.0467.

Num, number; LED, light-emitting diode; N/A, not applicable.

Given this study’s reliance on self-reported data from a single source, the potential for CMV to affect the results was a key consideration. To address this issue systematically, the research adopted a two-pronged approach, following the precedent of Zhang et al (2020). This approach combines proactive procedural remedies during the survey design with post-hoc statistical analyses, as recommended by Podsakoff et al (2003).

First, several procedural remedies were implemented to minimize CMV. Items were selected from established and validated scales, then reviewed by a panel of academic and industry experts to ensure their clarity, relevance, and appropriateness for the Chinese industrial context. For items originally developed in English, a standard back-translation procedure was employed to guarantee conceptual equivalence. Furthermore, the questionnaire was organized into three distinct sections (internal, supplier, and customer focus) to create psychological separation between the constructs for respondents.

Second, after data collection, two post-hoc statistical tests were performed

using the IBM SPSS Statistics software package (Version 26.0; IBM Corp., Armonk,

NY, USA). As an initial diagnostic, Harman’s single-factor test was conducted. An

exploratory factor analysis containing all items revealed that the first

unrotated factor accounted for 36.261% of the total variance. This value is well

below the 50% threshold (Podsakoff and Organ, 1986), providing preliminary

evidence that a single method factor was not a pervasive issue. For a more

rigorous assessment, a confirmatory factor analysis (CFA) was subsequently

conducted to compare the fit of the proposed eight-factor measurement model

against a single-factor model. The results confirmed that the eight-factor model

(the comparative fit index (CFI) = 0.908, the Tucker-Lewis index (TLI) = 0.894,

the root mean square error of approximation (RMSEA) = 0.072, and the standardized

root mean square residual (SRMR) = 0.075, the ratio of chi-square to degrees of

freedom (

Research has noted a growing trend in studies that explicitly tackle endogeneity, yet significant challenges remain, particularly within the framework of cross-sectional data (Lu et al, 2018). Scholars have outlined three main approaches to mitigate endogeneity in observational research: employing control variables, using instrumental variables (IV), and leveraging comparable units. The inclusion of control variables, in particular, has been widely utilized, with prior work adjusting for elements like seasonal patterns, temporal trends, and marketing efforts to limit endogeneity in cross-sectional settings (Lu et al, 2018).

Following this strategy, we incorporated several control variables into our model to account for firm and supply chain heterogeneity that could otherwise confound the results. Specifically, we controlled for firm age, ownership structure, industry sector, and firm size, which was operationalized using the number of employees, fixed assets, and annual sales. These variables were included because they can systematically influence a firm’s resource allocation and its propensity to adopt strategic initiatives like GSC practices.

While the inclusion of these controls helps to reduce potential biases, we acknowledge that it does not eliminate all endogeneity concerns. We address this issue transparently as a limitation of the study in the concluding section and suggest avenues for future research using alternative methodological approaches.

In his critique of reliability estimation, Cho (2016) argued that conventional approaches often lack methodological rigor. He therefore he developed a psychometrically grounded framework advocating coefficient selection based on explicit data characteristics. This framework systematically evaluates congeneric, tau-equivalent, and parallel coefficients to provide a more precise estimate of reliability.

Following this advanced paradigm, we first confirmed the unidimensionality of each construct via CFA, a necessary precondition for accurate reliability estimation. We then employed the RelCalc tool (Version 5.1; T-Cubed Systems, Inc., Westlake Village, CA, USA) to compute the most appropriate reliability estimate for our data. Through rigorous construct definition and standardized analysis procedures, the congeneric reliability coefficient emerged as the psychometrically appropriate estimate given our measurement architecture (see Table 3).

| Constructs (latent variables) | Parallel reliability | Tau-equivalent reliability | Congeneric reliability |

| Management support | 0.9292 | 0.9288 | 0.9293 |

| Financial support | 0.9023 | 0.9026 | 0.9072 |

| Internal e-linkage | 0.8801 | 0.8793 | 0.8803 |

| Supplier e-linkage | 0.8970 | 0.8961 | 0.8938 |

| Customer e-linkage | 0.9156 | 0.9141 | 0.9104 |

| Internal green practices | 0.8928 | 0.8919 | 0.8901 |

| Supplier green practices | 0.8997 | 0.8985 | 0.9019 |

| Customer green practices | 0.9361 | 0.9359 | 0.9367 |

The reliability and validity of the measurement model were rigorously assessed. Internal consistency reliability was confirmed, as the Cronbach’s alpha for each construct exceeded the conventional threshold. Content validity was established through two procedures. First, all measurement items were adapted from established scales in prior literature. Second, the instrument was reviewed and refined by a panel of senior international researchers to ensure clarity and relevance. Convergent validity was evaluated by examining standardized factor loadings, composite reliability (CR), and average variance extracted (AVE). As detailed in Table 4, all indicators provided strong evidence for convergent validity. Finally, discriminant validity was confirmed using the Fornell-Larcker criterion. This criterion requires that the square root of each construct’s AVE be greater than its correlation with any other construct. As shown in Table 5, this condition was met for all constructs in the model, indicating adequate discriminant validity.

| Items | Factor loadings | References | ||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | Mean | SD | |||

| MS: Management support: | ||||||||||||

| Top management commitment | 0.866 | 4.673 | 1.674 | Zhu et al (2008); | ||||||||

| Middle-level manage’s support for green supply chain management | 0.909 | 4.607 | 1.699 | Green et al (2019); | ||||||||

| Cross-departments cooperation to improve the environment | 0.858 | 4.645 | 1.559 | Tseng et al (2019) | ||||||||

| Total environmental quality management | 0.807 | 4.886 | 1.579 | |||||||||

| Environmental requirements and audit procedures | 0.786 | 4.919 | 1.723 | |||||||||

| FS: Financial support: | ||||||||||||

| Increasing total environmental investment | 0.800 | 5.365 | 1.209 | Zhu and Sarkis (2006); | ||||||||

| Increasing environment operating investment | 0.925 | 5.403 | 1.224 | Walker et al (2008); | ||||||||

| Increasing environment training investment | 0.938 | 5.232 | 1.283 | Sarpong and Oppong (2023); | ||||||||

| Increasing procurement of environmentally friendly materials | 0.682 | 5.294 | 1.234 | Agyemang et al (2018) | ||||||||

| IEI: Internal e-linkage: | ||||||||||||

| Data and information integration between functional departments within the firm | 0.815 | 4.967 | 1.442 | Ganbold et al (2021); | ||||||||

| Application software systems integration between functional departments | 0.863 | 4.976 | 1.617 | Liu et al (2015); | ||||||||

| Integrated inventory management | 0.755 | 5.213 | 1.479 | Huo (2012); | ||||||||

| Real time inventory tracking | 0.708 | 5.175 | 1.455 | Frohlich (2002) | ||||||||

| Real-time tracking of logistics and service data | 0.613 | 4.995 | 1.554 | |||||||||

| SEI: Supplier e-linkage(upstream): |

||||||||||||

| Integrating communication systems with suppliers | 0.782 | 3.550 | 1.821 | |||||||||

| Trading with our major suppliers by IT | 0.905 | 3.882 | 1.732 | |||||||||

| Delivering purchase orders and funds to our suppliers with integrated IT systems | 0.729 | 4.261 | 1.722 | |||||||||

| Tracking and accelerating shipments from suppliers with the integrated IT systems | 0.819 | 4.142 | 1.756 | |||||||||

| CEI: Customer e-linkage(downstream): |

||||||||||||

| Integrating communication systems with customers | 0.803 | 3.791 | 1.873 | |||||||||

| We trade with our major customers by IT | 0.891 | 4.175 | 1.935 | |||||||||

| Delivering purchase orders and funds to our customers with integrated IT systems | 0.814 | 4.502 | 1.749 | |||||||||

| Tracking and accelerating shipments from customers with integrated IT systems | 0.837 | 4.469 | 1.733 | |||||||||

| IGP: Internal Green Practices: | ||||||||||||

| Investing in excess inventory/raw material recovery | 0.693 | 4.630 | 1.739 | Zhu et al (2017b); | ||||||||

| Selling waste debris and materials | 0.585 | 4.682 | 1.667 | Schmidt et al (2017); | ||||||||

| Selling superfluous equipment | 0.656 | 4.445 | 1.702 | Acquah et al (2021); | ||||||||

| Relevant product design to reduce material/energy consumption | 0.862 | 4.806 | 1.542 | Wang et al (2018) | ||||||||

| Designing for components and parts recycling | 0.859 | 4.483 | 1.752 | |||||||||

| Designing related products to reduce harmful emissions | 0.839 | 4.649 | 1.645 | |||||||||

| SGP: Supplier Green Practices: |

||||||||||||

| Providing design specifications for purchasing materials to meet environmental requirements to suppliers | 0.675 | 4.711 | 1.459 | |||||||||

| Working with major suppliers for environmental goals | 0.695 | 4.512 | 1.478 | |||||||||

| Environmental audit of the internal management of suppliers | 0.899 | 4.265 | 1.745 | |||||||||

| ISO 14001 certification of suppliers | 0.744 | 4.659 | 1.726 | |||||||||

| Environmental friendly activities of secondary suppliers | 0.903 | 4.261 | 1.744 | |||||||||

| CGP: Customer Green Practices: |

||||||||||||

| Collaborating with key customers for eco-design | 0.901 | 4.166 | 1.646 | |||||||||

| Working with major customers for cleaner production | 0.939 | 4.242 | 1.686 | |||||||||

| Collaborating with major customers for green packaging | 0.857 | 4.451 | 1.651 | |||||||||

| Working together for environmental goals | 0.851 | 4.412 | 1.532 | |||||||||

Scale: Totally disagreed–totally agreed (1–7).

CFA, confirmatory factor analysis; CR, composite reliability; AVE, average variance extracted; SD, standard deviation.

| Construct | MEAN | S.D. | 1. | 2. | 3. | 4. | 5. | 6. | 7. | 8. |

| 1. MS | 4.746 | 1.454 | 0.845 | |||||||

| 2. FS | 5.324 | 1.089 | 0.421*** | 0.772 | ||||||

| 3. IEI | 5.065 | 1.241 | 0.389*** | 0.343*** | 0.832 | |||||

| 4. SEI | 3.959 | 1.535 | 0.324*** | 0.237*** | 0.420*** | 0.849 | ||||

| 5. CEI | 4.235 | 1.627 | 0.172** | 0.190** | 0.272*** | 0.631*** | 0.762 | |||

| 6. IGP | 4.616 | 1.350 | 0.573*** | 0.368*** | 0.316*** | 0.422*** | 0.341*** | 0.808 | ||

| 7. SGP | 4.482 | 1.379 | 0.629*** | 0.422*** | 0.410*** | 0.503*** | 0.277*** | 0.519*** | 0.893 | |

| 8. CGP | 4.319 | 1.493 | 0.397*** | 0.354*** | 0.347*** | 0.486*** | 0.437*** | 0.452*** | 0.574*** | 0.785 |

Notes: **p

Structural equation modeling was conducted using Mplus software (Version 7.4;

Muthén & Muthén, Los Angeles, CA, USA) with maximum likelihood

estimation to assess the theoretical model paths. The measurement model

demonstrated acceptable fit:

| Dependent variables | |||||||

| Supplier green practices | Internal green practices | Customer green practices | |||||

| Coefficients | p value | Coefficient | p value | Coefficient | p value | ||

| Control variables | YEAR | –0.019 | 0.802 | 0.178*** | 0.001 | –0.009 | 0.912 |

| OWNERSHIP | 0.147** | 0.012 | –0.041 | 0.490 | 0.050 | 0.433 | |

| EMPLOYEES | 0.090 | 0.384 | –0.063 | 0.549 | –0.218** | 0.048 | |

| INDUSTRY | 0.023 | 0.697 | 0.038 | 0.526 | –0.051 | 0.427 | |

| FIXED ASSETS | 0.117 | 0.220 | 0.120 | 0.214 | 0.302** | 0.003 | |

| ANNUAL SALES | –0.045 | 0.626 | –0.067 | 0.473 | –0.030 | 0.762 | |

| Independent variables | MS | 0.530*** | 0.000 | 0.522*** | 0.000 | 0.311*** | 0.000 |

| FS | 0.179** | 0.009 | 0.175** | 0.012 | 0.256*** | 0.000 | |

Model fit information: the comparative fit index(CFI) = 0.908, the Tucker-Lewis index (TLI) = 0.894, the root mean square error of approximation (RMSEA) = 0.072, the standardized root mean square residual (SRMR) = 0.076,

the ratio of chi-square to degrees of freedom (

Notes: **p

To test the moderating effects, this study moved beyond traditional product-indicator (PI) approaches, which are often limited by non-normality issues and complex constraints. Instead, we adopted the Latent Moderated Structural Equations (LMS) method. Following the methodological guidelines of (Kelava et al, 2011), the LMS framework was selected for its robust performance in models with multiple latent variables and its reliable implementation in Mplus 7.4.

The results from the LMS analysis are presented in Table 7. The moderating

effects involving financial support were largely statistically insignificant. The

sole exception was a positive and marginally significant interaction between

supplier e-linkage and financial support on internal green practices (

| Supplier e-linkage as a moderating variable(1) | |||||||||||

| Dependent variables | |||||||||||

| SGP | IGP | CGP | |||||||||

| Coefficients | S.E. | p value | Coefficient | S.E. | p value | Coefficient | S.E. | p value | |||

| Control variables | YEAR | 0.010 | 0.072 | 0.890 | 0.167** | 0.072 | 0.021 | 0.011 | 0.079 | 0.892 | |

| OWNERSHIP | 0.151** | 0.057 | 0.008 | –0.029 | 0.057 | 0.604 | 0.046 | 0.062 | 0.464 | ||

| EMPLOYEES | 0.069 | 0.100 | 0.491 | –0.056 | 0.100 | 0.579 | –0.223* | 0.109 | 0.040 | ||

| INDUSTRY | –0.004 | 0.058 | 0.947 | 0.045 | 0.058 | 0.435 | –0.060 | 0.063 | 0.340 | ||

| FIXED ASSETS | 0.133 | 0.092 | 0.150 | 0.101 | 0.093 | 0.276 | 0.309** | 0.101 | 0.002 | ||

| ANNUAL SALES | –0.091 | 0.090 | 0.313 | –0.029 | 0.092 | 0.751 | –0.068 | 0.100 | 0.498 | ||

| Independent variables | MS | 0.524*** | 0.071 | 0.000 | 0.514*** | 0.069 | 0.000 | 0.264** | 0.084 | 0.002 | |

| FS | 0.230*** | 0.071 | 0.001 | 0.207** | 0.071 | 0.003 | 0.302*** | 0.077 | 0.000 | ||

| Interaction variables | MS |

–0.153** | 0.072 | 0.034 | 0.103 | 0.071 | 0.146 | –0.177** | 0.078 | 0.024 | |

| FS |

0.081 | 0.072 | 0.256 | 0.120* | 0.070 | 0.086 | 0.096 | 0.077 | 0.211 | ||

| Internal e-linkage as a moderating variable(2) | |||||||||||

| Control variables | YEAR | 0.005 | 0.072 | 0.947 | 0.155** | 0.072 | 0.032 | 0.001 | 0.080 | 0.994 | |

| OWNERSHIP | 0.157** | 0.057 | 0.006 | –0.051 | 0.057 | 0.370 | 0.052 | 0.063 | 0.413 | ||

| EMPLOYEES | 0.058 | 0.102 | 0.571 | –0.025 | 0.102 | 0.804 | –0.231** | 0.110 | 0.037 | ||

| INDUSTRY | 0.000 | 0.058 | 0.998 | 0.048 | 0.058 | 0.406 | –0.053 | 0.064 | 0.405 | ||

| FIXED ASSETS | 0.143 | 0.093 | 0.125 | 0.088 | 0.092 | 0.348 | 0.314** | 0.102 | 0.002 | ||

| ANNUAL SALES | –0.078 | 0.091 | 0.392 | –0.032 | 0.091 | 0.725 | –0.048 | 0.101 | 0.631 | ||

| Independent variables | MS | 0.542*** | 0.069 | 0.000 | 0.538*** | 0.067 | 0.000 | 0.309*** | 0.082 | 0.000 | |

| FS | 0.202** | 0.070 | 0.004 | 0.168** | 0.071 | 0.018 | 0.256*** | 0.077 | 0.001 | ||

| Interaction variables | MS |

–0.086 | 0.076 | 0.254 | 0.184** | 0.083 | 0.026 | –0.055 | 0.089 | 0.539 | |

| FS |

0.013 | 0.074 | 0.860 | 0.002 | 0.080 | 0.978 | –0.016 | 0.084 | 0.849 | ||

| Customer e-linkage as a moderating variable(3) | |||||||||||

| Control variables | YEAR | –0.005 | 0.071 | 0.943 | 0.182** | 0.074 | 0.013 | –0.005 | 0.079 | 0.949 | |

| OWNERSHIP | 0.152** | 0.057 | 0.007 | –0.037 | 0.059 | 0.532 | 0.047 | 0.063 | 0.456 | ||

| EMPLOYEES | 0.080 | 0.100 | 0.425 | –0.065 | 0.104 | 0.531 | –0.209* | 0.109 | 0.056 | ||

| INDUSTRY | –0.002 | 0.058 | 0.972 | 0.040 | 0.060 | 0.500 | –0.054 | 0.064 | 0.397 | ||

| FIXED ASSETS | 0.133 | 0.092 | 0.148 | 0.124 | 0.096 | 0.196 | 0.306** | 0.101 | 0.002 | ||

| ANNUAL SALES | –0.069 | 0.090 | 0.444 | –0.074 | 0.094 | 0.432 | –0.050 | 0.100 | 0.619 | ||

| Independent variables | MS | 0.545*** | 0.066 | 0.000 | 0.523*** | 0.068 | 0.000 | 0.306*** | 0.078 | 0.000 | |

| FS | 0.195** | 0.067 | 0.003 | 0.180** | 0.069 | 0.009 | 0.265*** | 0.072 | 0.000 | ||

| Interaction variables | MS |

–0.165** | 0.068 | 0.016 | –0.028 | 0.074 | 0.701 | –0.144* | 0.080 | 0.072 | |

| FS |

0.081 | 0.069 | 0.242 | 0.030 | 0.074 | 0.687 | 0.113 | 0.081 | 0.162 | ||

Model fit information:

(1) Information Criteria: Akaike (AIC)- 18,036.369; Bayesian (BIC)- 18,438.592; Sample-Size Adjusted BIC- 18,058.358; Number of Free Parameters 120.

(2) Information Criteria: Akaike (AIC)- 18,605.677; Bayesian (BIC)- 19,017.955; Sample-Size Adjusted BIC- 18,628.215; Number of Free Parameters 120.

(3) Information Criteria: Akaike (AIC)- 18,071.729; Bayesian (BIC)- 18,473.952; Sample-Size Adjusted BIC- 18,093.718; Number of Free Parameters 120.

Notes:

Unlike standard SEM, LMS uses the full information contained in the raw data, not just the means and covariances, which shows the standardized coefficients in the results after Mplus 7.4.

*p

LMS, Latent Moderated Structural Equations; SEL, supplier e-linkage; IEL, internal e-linkage; CEL, customer e-linkage; S.E., Standard Error.

In contrast, the moderating effects involving management support were more

pronounced and varied. The analysis revealed a predominantly antagonistic pattern

for external e-linkages. Specifically, supplier e-linkage significantly weakened

the effect of management support on both supplier green practices (

In sum, this complex pattern of results provides partial support for both the synergistic (H3) and antagonistic (H4) hypotheses, suggesting a nuanced role for supply chain e-linkage. A detailed interpretation of these findings is reserved for the discussion section. A full summary of the hypothesis tests is provided in Table 8.

| Hypothesis | Interaction term | Dependent variable | Coefficient | Conclusion | |

| Synergistic effect | H3a(1) | MS |

SGP/IGP/CGP | - | Not Supported |

| H3a(2) | MS |

IGP | 0.184** | Supported | |

| H3a(3) | MS |

SCP/CGP | - | Not Supported | |

| H3a(4) | MS |

SGP/IGP/CGP | - | Not Supported | |

| H3b(1) | FS |

IGP | 0.120* | Supported | |

| H3b(2) | FS |

SGP/CGP | - | Not Supported | |

| H3b(3) | FS |

SGP/IGP/CGP | - | Not Supported | |

| H3b(4) | FS |

SGP/IGP/CGP | - | Not Supported | |

| Antagonistic effect | H4a(1) | MS |

SGP | –0.153** | Supported |

| H4a(2) | MS |

CGP | –0.177** | Supported | |

| H4a(3) | MS |

IGP | - | Not Supported | |

| H4a(4) | MS |

SGP/IGP/CGP | - | Not Supported | |

| H4a(5) | MS |

SGP | –0.165** | Supported | |

| H4a(6) | MS |

IGP | - | Not Supported | |

| H4a(7) | MS |

CGP | –0.144* | Supported | |

| H4b(1) | FS |

SGP/IGP/CGP | - | Not Supported | |

| H4b(2) | FS |

SGP/IGP/CGP | - | Not Supported | |

| H4b(3) | FS |

SGP/IGP/CGP | - | Not Supported |

Notes: *p

This study examines the distinct roles of management support and financial support in driving GSC practices. Our analysis reveals that management support has a consistently positive and significant impact across all three dimensions of GSC: supplier, internal, and customer practices. This result empirically confirms the theoretical link between strategic environmental management commitment and GSC implementation proposed by Diabat and Govindan (2011), aligning with prior findings (Huang et al, 2017; Walker et al, 2008). Financial support is also found to be a critical driver of GSC practices, aligning with recent evidence (Wang et al, 2018). This finding helps to resolve a theoretical ambiguity noted by Liu et al (2012), underscoring that while managerial commitment is essential, it cannot substitute for dedicated capital investment in GSC initiatives. Notably, a key finding is that management support has a significantly stronger effect on GSC practices than financial support.

Having established that internal resources like management and financial support are direct and significant drivers of GSC practices, we argue that their ultimate effectiveness is contingent upon the inter-organizational context in which a firm operates. Drawing from the competing logics of the RBV and RDT, we propose that the moderating effect of e-linkage is paradoxical. We therefore test whether supply chain e-linkage strengthens (a synergistic effect) or weakens (an antagonistic effect) the positive influence of a firm’s internal resources on its GSC practices.

The results first provide clear evidence for a synergistic effect within the

firm’s own boundaries. The analysis revealed that internal e-linkage (IEL)

significantly strengthens the positive relationship between management support

and internal green practices (

A second, more nuanced synergistic effect emerged in an external context. The

analysis showed a positive and significant interaction between supplier e-linkage

(SEL) and financial support on internal green practices (

The findings reveal the “dark side” when e-linkage crosses organizational boundaries. This antagonistic effect, which provides partial support for H4a, was observed exclusively in the relationship with management support and aligns with the core logic of RDT. RDT posits that high integration can lead to dependency, which in turn creates power imbalances and makes a firm vulnerable to partners’ opportunistic or adversarial behavior (Caniëls and Gelderman, 2007; McDonald, 1999).

The analysis first revealed a supplier-driven antagonistic effect. Specifically,

SEL significantly attenuated the positive impact of management support on both

supplier green practices (

A similar antagonistic pattern was driven by customer power, a critical

component of supply chain relationships (Zhao et al, 2008). The analysis

showed that customer e-linkage (CEL) significantly weakened the relationship

between management support and supplier green practices (

This study makes several contributions to the GSCM and organizational theory literature. First, by empirically examining both management and financial support, this research clarifies their distinct and complementary roles. Our finding that management support has a stronger direct effect, coupled with the confirmation that firm-level financial support is also a significant driver, provides a more complete picture of the internal resources necessary for GSC practices. This addresses calls in the literature to move beyond purely managerial perspectives and incorporate financial considerations.

More significantly, this study contributes by unpacking the complex interplay between internal capabilities and external dependencies in the digital era. We do so by integrating two foundational but often competing theories: the RBV, which focuses on internal value creation, and RDT, which emphasizes external constraints.

Our findings first challenge a simplistic application of RDT. Consistent with RDT’s core tenet, our results confirm that external e-linkage can become a conduit for power imbalances, where dependency on suppliers or customers weakens the effectiveness of a firm’s managerial efforts (Pfeffer and Salancik, 1978). This is the “dark side” of integration, where partners may engage in opportunistic behavior, creating hold-up problems that threaten the firm’s green initiatives. However, our study extends RDT by illuminating a sophisticated, agentic response to these dependency risks. The “strategic buffer” finding—where firms channel financial support internally in response to high supplier dependency—is not predicted by traditional RDT models, which often focus on external strategies like forming alternative alliances or mergers. This finding suggests that firms can internalize their response to external threats. They strategically deploy fungible resources (capital) to build idiosyncratic internal capabilities (green processes), thereby mitigating the threat of value appropriation by a powerful partner. This adds a critical, proactive, and internal risk-management dimension to RDT’s portfolio of dependency-management strategies (Hillman et al, 2009).

Concurrently, we provide a more dynamic perspective on the RBV. While RBV posits that competitive advantage stems from valuable, rare, and inimitable internal resources (Barney, 1991), it has been criticized for under-emphasizing the external environment’s role in shaping which resources become valuable. Our findings provide a direct link. The synergistic effect of internal e-linkage confirms the RBV logic that well-orchestrated internal capabilities drive performance. More importantly, the “strategic buffer” finding demonstrates how external relational pressures (an RDT concern) can act as a direct catalyst for the development of valuable internal resources (an RBV outcome). In this way, RDT provides a crucial “why” for RBV’s “what”—firms develop these specific internal green capabilities precisely because they face external dependency risks that threaten the rent-generating potential of their green strategies.

Our findings also yield several actionable insights for managers. First, the results underscore that managerial commitment alone is insufficient. While strong leadership is the primary driver, it must be complemented by dedicated financial investment to effectively implement GSC practices. Managers should therefore advocate for and secure specific budgets for green initiatives rather than assuming that managerial directives will suffice.

Second, managers must treat supply chain e-linkage as a double-edged sword. The practical advice is to differentiate their approach based on the relationship’s context. They should proactively leverage internal e-linkage as a tool to improve communication and enhance the efficiency of their management systems. However, they should approach external e-linkages with strategic caution, recognizing them as settings of cooperative tension where dependency can shift bargaining power.

Finally, our findings offer a specific, counter-intuitive strategy for managing supply chain dependency. The conventional response to a powerful partner might be to increase monitoring or seek alternative partners. Our results suggest a third way: strategic internal investment. When faced with high dependency on a critical supplier, managers can allocate financial resources to bolster their own internal green capabilities. This action serves as a practical hedge, creating an internal buffer that ensures operational autonomy and safeguards the firm’s environmental performance, regardless of the partner’s actions.

This study’s limitations offer several promising avenues for future research. First, our focus on manufacturing firms in China, while appropriate for a context of rapid economic growth, may constrain the generalizability of our findings. Future research could test the proposed model in different institutional and cultural contexts to explore its boundary conditions. Second, the cross-sectional design provides a static snapshot of the relationships under investigation. It cannot fully capture their dynamic evolution over time. Longitudinal studies would therefore be invaluable for observing how the synergistic and antagonistic effects of e-linkage shift as inter-firm relationships mature. Third, by focusing solely on the focal firm’s perspective, our study does not capture the full complexity of inter-organizational dynamics. Future research adopting a dyadic or triadic design could provide a more comprehensive understanding of how power imbalances and relational tensions are perceived by all parties involved. Finally, while our model includes several control variables, the potential for endogeneity cannot be fully ruled out.

The datasets generated during and analyzed during the current study are available from the corresponding author on reasonable request.

JZ contributed to the conceptualization, original draft writing, and validation. JD was responsible for data curation, formal analysis, and review and editing of the manuscript. XL developed the methodology and contributed to the writing, review, and editing of the paper. All authors read and approved the final manuscript. All authors have participated sufficiently in the work and agreed to be accountable for all aspects of the work.

We gratefully acknowledge the valuable support and guidance provided by Professor Zhang from Zhongnan University of Economics and Law throughout the course of this research.

This study was funded by Hubei Provincial Social Science Fund Project (HBSKJJ20233257), the Philosophy and Social Science Research Project (21Q085) of the Hubei Provincial Department of Education, and the Doctoral Starting up Foundation of Hubei University of Technology (XJKY20220057).

The authors declare no conflict of interest.

During the preparation of this work the authors used Gemini 2.5 pro in order to check spell and grammar. After using this tool, the authors reviewed and edited the content as needed and takes full responsibility for the content of the publication.

See Table 9.

| Item Description | MS | IGP | CGP | IEL | SGP | FS | CEI | SEI | |

| Management Support (MS) | |||||||||

| Top management commitment | 0.800 | ||||||||

| Middle-level manager’s support for green supply chain management | 0.853 | ||||||||

| Cross-deparments cooperation to improve the environment | 0.728 | ||||||||

| Total environmental quality management | 0.809 | ||||||||

| Environmental requirements and audit procedures | 0.729 | ||||||||

| Internal Green Practices (IGP) | |||||||||

| Investing in excess inventory/raw material recovery | 0.602 | ||||||||

| Selling waste debris and materials | 0.766 | ||||||||

| Selling superfluous equipment | 0.765 | ||||||||

| Relevant product design to reduce materia/energy consumption | 0.735 | ||||||||

| Designing for components and parts recycling | 0.766 | ||||||||

| Designing related products to reduce harmful emissions | 0.715 | ||||||||

| Customer Green Practices (CGP) | |||||||||

| Collaborating with key customers for eco-design | 0.817 | ||||||||

| Working with major customers for cleaner production | 0.830 | ||||||||

| Collaborating with major customers for green packaging | 0.811 | ||||||||

| Working together for environmental goals | 0.809 | ||||||||

| Internal E-linkage (IEL) | |||||||||

| Data and information integration between functional departments within the firm | 0.742 | ||||||||

| Application software systems integration between functional departments | 0.774 | ||||||||

| Integrated inventory management | 0.809 | ||||||||

| Real time inventory tracking | 0.807 | ||||||||

| Real-time tracking of logistics and service data | 0.742 | ||||||||

| Supplier Green Practices (SGP) | |||||||||

| Providing design specifications for purchasing materials to meet environmental requirements to suppliers | 0.564 | ||||||||

| Working with major suppliers for environmental goals | 0.634 | ||||||||

| Environmental audit of the internal management of suppliers | 0.664 | ||||||||

| ISO 14001certification of suppliers | 0.778 | ||||||||

| Environmental friendly activities of secondary suppliers | 0.663 | ||||||||

| Financial Support (FS) | |||||||||

| Increasing total environmental investment | 0.792 | ||||||||

| Increasing environment operating investment | 0.868 | ||||||||

| Increasing environment training investment | 0.874 | ||||||||

| Increasing procurement of environmentally friendly materials | 0.774 | ||||||||

| Customer E-linkage (CEI) | |||||||||

| Integrating communication systems with customers | 0.822 | ||||||||

| We trade with our major customers by IT | 0.807 | ||||||||

| Delivering purchase orders and funds to our customers with integrated IT systems | 0.874 | ||||||||

| Tracking and accelerating shipments from customers with integrated IT systems | 0.854 | ||||||||

| Supplier E-linkage (SEI) | |||||||||

| Integrating communication systems with suppliers | 0.522 | ||||||||

| Trading with our major suppliers by IT | 0.672 | ||||||||

| Delivering purchase orders and funds to our suppliers with integrated IT systems | 0.763 | ||||||||

| Tracking and accelerating shipments from suppliers with the integrated IT systems | 0.777 | ||||||||

Notes: Extraction Method: Principal Axis Factoring. Rotation Method: Direct Oblimin with Kaiser Normalization. Loadings under 0.40 are suppressed for clarity. Kaiser-Meyer-Olkin (KMO) = 0.876; Bartlett’s Test of Sphericity approx.

References

Publisher’s Note: IMR Press stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.